| © 2025 Zacks Investment Research, All Rights Reserved | 101 N Wacker Drive, Floor 15, Chicago, IL 60606 |

| Zacks Equity Research | www.zacks.com | Page $[page] of $[total] |

|

Zacks Report Date: August 30, 2025 |

Deere & Company (DE)$478.64 (Stock Price as of 08/29/2025) Price Target (6-12 Months): $380.00 |

|

||||||||||||||||

Summary

Deere is witnessing solid growth in order levels, which is expected to aid its top-line performance in the forthcoming quarters. Strong replacement demand will continue to boost the company's results. Demand for its construction equipment will likely benefit from anticipated growth in infrastructural investments in the United States. However, inflated material and labor costs are anticipated to impact the company's margins. Supply chain challenges also remain a woe. Nonetheless, the company's efforts to improve pricing will somewhat help offset these headwinds. Product launches equipped with the latest technology to make farming automated will continue to provide Deere with an edge over its competitors. The company is poised to benefit in the long run from rapid growth in the global population and rising worldwide infrastructure needs.

Data Overview

| 52 Week High-Low | $533.78 - $378.45 |

|---|---|

| 20 Day Average Volume (sh) | 1,456,507 |

| Market Cap | $129.6 B |

| YTD Price Change | 13.0% |

| Beta | 1.06 |

| Dividend / Div Yld | $6.48 / 1.4% |

| Industry | Manufacturing - Farm Equipment |

| Zacks Industry Rank | Bottom 13% (212 out of 245) |

| Last EPS Surprise | 2.8% |

|---|---|

| Last Sales Surprise | 1.0% |

| EPS F1 Est- 4 week change | -1.2% |

| Expected Report Date | 11/20/2025 |

| Earnings ESP | -0.4% |

| P/E TTM | 25.0 |

|---|---|

| P/E F1 | 17.3 |

| PEG F1 | NA |

| P/S TTM | 2.9 |

Price, Consensus & Surprise(1)

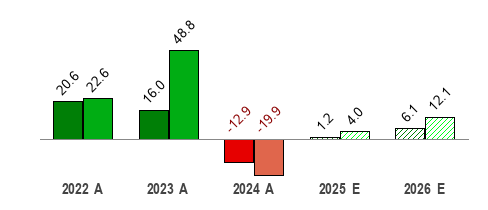

Sales and EPS Growth Rates (Y/Y %)(2)

Sales  |

EPS  |

Sales Estimates (millions of $)(2)

| Q1 | Q2 | Q3 | Q4 | Annual* | |

|---|---|---|---|---|---|

2026 |

|||||

2025 |

6,809 A |

11,171 A |

10,357 A |

12,259 E |

48,997 E |

2024 |

10,486 A |

13,610 A |

11,387 A |

9,275 A |

44,759 A |

EPS Estimates(2)

| Q1 | Q2 | Q3 | Q4 | Annual* | |

|---|---|---|---|---|---|

2026 |

|||||

2025 |

3.19 A |

6.64 A |

4.75 A |

7.39 E |

28.85 E |

2024 |

6.23 A |

8.53 A |

6.29 A |

4.55 A |

25.62 A |

*Quarterly figures may not add up to annual.

1) The data in the charts and tables, except the estimates, is as of 08/29/2025.

2) The report's text, the analyst-provided estimates, and the price target are as of 12/06/2023.

Overview

As of 12/06/2023

Illinois-based Deere is the world’s largest producer of agricultural equipment, manufacturing agricultural machinery since 1837 under the iconic John Deere brand with its signature green and yellow color scheme. It is the 81st-largest company in the S&P 500 Index with a market capitalization of around $106 billion. It has an advantage in most farm machinery categories as its machines come with advanced features and are better constructed than its competitors. Deere is currently the world leader in precision agriculture and remains focused on revolutionizing agriculture with technology, in an effort to make farming automated, easier and more precise across the production process.

Beginning fiscal 2021, the company has four reportable segments. Agriculture and turf operations had been divided into two new segments:

The Production and Precision Agriculture segment (48% of equipment revenues in fiscal 2023) is responsible for defining, developing, and delivering global equipment and technology solutions that cater to production-scale growers of large grains, small grains, cotton, and sugar. Primary products include large and certain mid-size tractors, combines, cotton pickers, sugarcane harvesters and loaders, and soil preparation, seeding, application and crop care equipment.

The Small Agriculture and Turf segment (25% of equipment revenues in fiscal 2023) will deliver products to support mid-size and small growers and producers globally, and turf customers. It will cater to production systems for dairy and livestock, high-value crops, and turf and utility operators. Products include certain mid-size and small tractors, and hay and forage equipment, riding and commercial lawn equipment, golf course equipment, and utility vehicles.

The Construction and Forestry (26% of equipment revenues in fiscal 2023) segment manufactures machines and service parts used in construction, earthmoving, material handling and timber harvesting. Deere also manufactures and distributes road building equipment through its wholly-owned subsidiaries of the Wirtgen Group.

Deere also finances sales and leases for new and used equipment through its Financial Services segment, which generated 8% of the Deere’s revenues in fiscal 2023.

As of 08/29/2025

Reasons To Buy:

Demand in agricultural and construction sectors, acquisitions, focus on advanced technologies in products, expansion in precision agriculture and margin improvement plan will aid Deere's results.

The USDA (U.S. Department of Agriculture) projects net farm income at $141.3 billion for 2023, which is 23% lower than that reported in 2022. The decline is mainly due to lower direct government payments. Nevertheless, despite this decline, net farm income in 2023 will be higher than the 2003-2022 average. This will continue to support Deere’s margin. The farm size has been on the rise in the United States, which requires more laborers. Given the escalation in labor costs every year, farmers are resorting to farming equipment to replace labor. The U.S. agricultural machinery market is projected to reach $52.73 billion by 2027, seeing a CAGR of 3.3% over 2021-2027.

In the years to come, demand for agricultural equipment will be fueled by increased global demand for food, both from population growth and an increasing proportion of the population aspiring for better living standards. Drought and water scarcity issues in the United States and other parts of the world support the need for efficient irrigation.

Deere’s row-crop tractor orders are booked through most of the fiscal second quarter and four-wheel drive tractors are sold out through the end of the fiscal third quarter. Its order books are around 45% full. This reflects improved demand in its markets. The need to replace aging equipment will also support Deere’s top-line performance. Demand for its construction equipment will be supported by increased infrastructure spending.

Deere is assessing cost structure by reviewing organization efficiency and footprint assessment, which in turn will help improve margins. Its price realization action is expected to offset higher material and freight costs. Deere’s smart industrial strategy and is aiding customers manage escalating input costs while improving their yields. The company is focused on driving capital-allocation decisions, intensifying investments in precision agriculture, as well as enhancing capabilities in aftermarket and retrofit business. Deere has implemented actions to strengthen its financial position and preserve liquidity.

Deere remains well poised for growth over the long term, backed by steady investments in new products and geographies. The company will benefit from concerted focus on launching products with advanced technologies and features, which provides it a competitive edge. These investments will aid its customers achieve improved profitability, productivity, and sustainability through the effective use of technology. It remains focused on revolutionizing agriculture with technology in an effort to make farming automated, easy to use and more precise across the production process.

The company is seeing strong demand from its new product launches like ExactRate planter applied fertilizer systems and AutoPath. ExactRate signifies the precision application of fertilizer, while AutoPath leverages Deere's onboard technology linked to its operation center throughout a customer's entire production cycle. AutoPath will strengthen automated farming in the future with its new features and technologies as part of the company’s Precision Agriculture software package strategies. Deere also launched its groundbreaking See & Spray Ultimate in March 2022. It can identify the difference between a weed and a healthy crop plant and only spray the weed and lower chemical usage.

Reasons To Sell:

Deere’s results will bear the impact of persistent supply-chain challenges, which are affecting production levels and delivery schedules. Higher costs and elevated debt level add to the concerns.

Deere has been affected by rising material, labor and logistical costs. Also supply-chain issues led to delays in deliveries of some parts, causing partially completed machinery to stack up at assembly plants as the company waited for the parts to arrive. This resulted in factories becoming less efficient lately. Consequently, overhead spend has also been high. Higher SG&A and R&D spend is also weighing on margins.

Deere’s small agricultural and turf equipment will continue to suffer from supply constraints, limiting industry production as well as higher material and freight costs. Equipment inventories remain well below normal and are unlikely to begin recovering in the upcoming quarter. In Europe, Agriculture and Turf segment as well as large agricultural equipment sales in U.S and Canada will continue to face supply-based constraints resulting in demand outstripping production for the year. These factors will continue to put pressure on the segment’s margins.

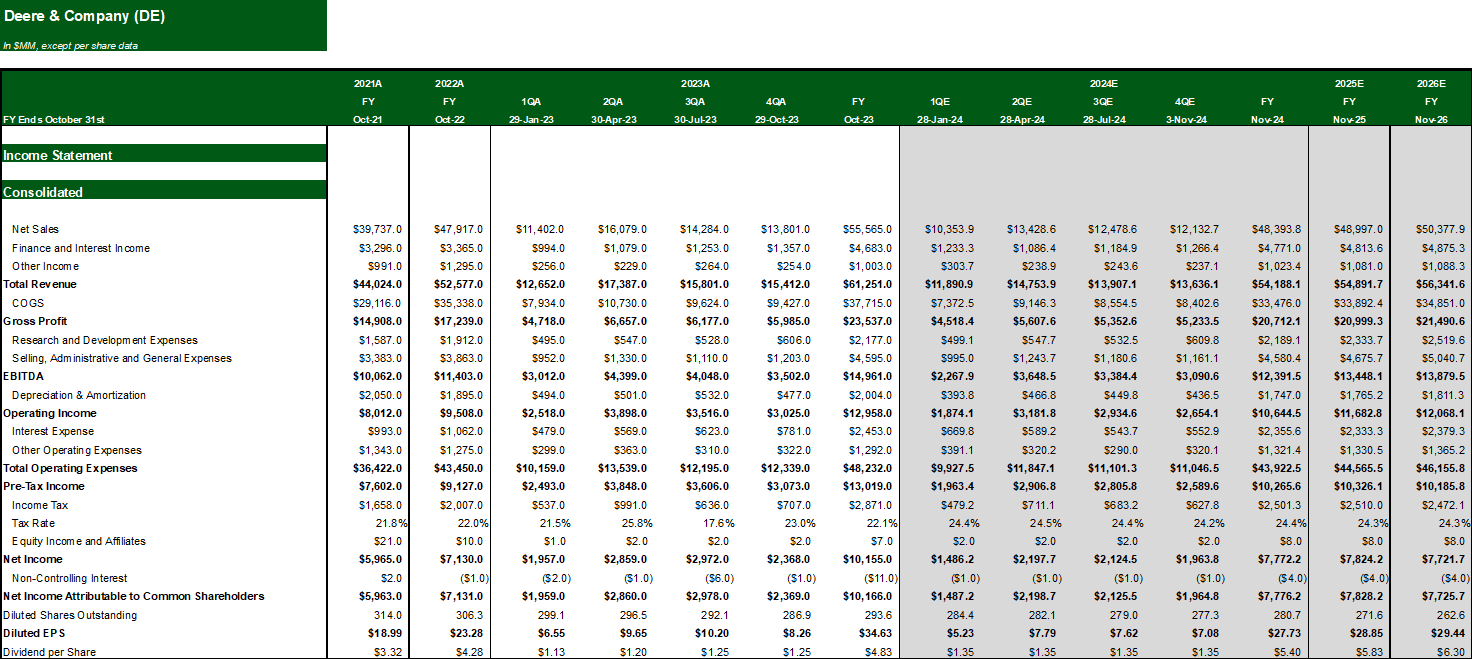

Deere expects net income for fiscal 2024 between $7.75 billion and $8.25 billion, stating that it expects volumes to return to mid-cycle levels. The stated range is much lower than net income, which is projected at $10.2 billion in fiscal 2023. Net sales for Production & Precision Agriculture are expected to be down 15-20% year over year in fiscal 2024. Sales of Small Agriculture & Turf are expected to decline in the range of 10-15%. Sales of Construction & Forestry are projected to be down 10%.

Over the last five fiscal years, Deere’s total debt increased, seeing a CAGR of 5.3%. The company’s times interest earned ratio is currently at 6.3. This is likely to weigh on the company’s growth.

Last Earnings Report

FY Quarter Ending |

10/31/2024 |

|---|

| Earnings Reporting Date | Aug 14, 2025 |

|---|---|

| Sales Surprise | 0.97% |

| EPS Surprise | 2.81% |

| Quarterly EPS | 4.75 |

| Annual EPS (TTM) | 19.13 |

Deere Q4 Earnings Beat, Shares Dip on Muted FY24 View

Deere reported fourth-quarter fiscal 2023 earnings of $8.26 per share, beating the Zacks Consensus Estimate of earnings of $7.49 per share. The bottom line increased 11% from the prior-year quarter’s levels, backed by favorable market conditions and price realization.

Despite the outperformance, DE shares dipped 5.3% in pre-market trading as the company’s fiscal 2024 guidance indicates a decline in sales in all its segments along with lower net income. The midpoint of the company’s provided range for net income indicates a year-over-year slump of 21%, thus reflecting the company’s expectations of weak demand.

Net sales of equipment operations (comprising Agriculture and Turf, Construction and Forestry) were $13,801 million, down 4% year over year. Revenues topped the Zacks Consensus Estimate of $13,628 million. Total net sales (including financial services and others) were $15,412 million, down 1% year over year.

Operational Update

The cost of sales in the reported quarter went down 7.7% year over year to $9,427 million. Total gross profit increased 5.7% year over year to $4,374 million. Selling, administrative and general expenses (SA&G) rose 1% to $1,203 million from the year-ago quarter levels.

Total operating profit (including financial services) was up 2% year over year to $3,025 million in the fiscal fourth quarter.

Segment Performance

The Production & Precision Agriculture segment’s sales declined 6% year over year to $6,965 million. The figure was higher than our model’s estimated revenues of $6,567 million for the quarter. Gains from price realization were offset by low volumes.

Operating profit increased 6% year over year to $1,836 million mainly due to price realization. Lower shipment volumes/sales mix, higher SA&G and research and development (R&D) expenses offset some of the gains. Our estimate for the segment’s operating profit was $1,677 million.

Small Agriculture & Turf sales were down 13% year over year at $3,739 million on low volumes, somewhat offset by price realization. Our projection for the segment’s sales was $3,175 million. Operating profit declined 12% year over year to $444 million. Lower sales, as well as elevated SA&G and R&D expenses, led to the decline. The figure was lower than our estimate of operating profit of $483 million for the segment.

Construction & Forestry sales were $3,742 million, up 11% year over year, backed by higher shipment volumes and price realization. The figure was lower than our projection of $3,772 million. Operating profit increased 25% year over year to $516 million. Gains from higher sales were partially offset by increased production costs, unfavorable impact of foreign currency exchange, less favorable sales mix and a loss on the sale of the Russian roadbuilding business. Our estimate for the segment’s operating profit was $678 million.

Revenues in Deere’s Financial Services division were $1,347 million in the reported quarter, up 36% year over year. The figure was higher than our estimate of $1,049 million. The segment’s operating income was $229 million in the quarter under review, down compared with $297 million in the last fiscal year’s comparable quarter. Our projection was $276 million for the quarter.

Net income for Financial services declined 18% year over year to $190 million in the fourth quarter of fiscal 2023.

Financial Update

Deere reported cash and cash equivalents of $7.46 billion at the end of fiscal 2023 compared with $4.77 billion recorded at fiscal 2022 end. Cash flow from operating activities was $8.6 billion in fiscal 2023 compared with $4.7 billion in the prior fiscal.

At the end of fiscal 2023, DE’s long-term borrowing was nearly $38.5 billion compared with $33.6 billion at fiscal 2022 end.

Fiscal 2023 Performance

The company reported earnings per share of $34.63 in fiscal 2023, which came in 49% higher than the earnings per share of $23.28 in fiscal 2022. It also surpassed the Zacks Consensus Estimate of earnings of $33.89 per share.

Net sales of equipment operations (comprising Agriculture and Turf, Construction and Forestry) rose 16% year over year to $55.6 billion, which beat the consensus estimate of $55.4 billion. Total net sales (including financial services and others) were $61.3 million, up 16.5% year over year.

Guidance

Deere expects net income for fiscal 2024 to be between $7.75 billion and $8.25 billion stating that it expects volumes to return to mid-cycle levels. The stated range is much lower than net income attributable of $10.2 billion in fiscal 2023.

Net sales for Production & Precision Agriculture are expected to be down 15-20% year over year in fiscal 2024. Sales of Small Agriculture & Turf are expected to decline in the range of 10% to 15%. Sales of Construction & Forestry are projected to be down 10%. The Financial Services segment’s net income is expected to be around $770 million.

Valuation

Deere’s shares are down 4.8% in the trailing six-month period and down 17% in the trailing 12-month period. Over the past six months, stocks in the Manufacturing - Farm Equipment industry and Industrial Products sector are down 6% and up 5%, respectively. Over the past year, the Zacks sub-industry are down 18.1% while the sector are down 7.5%.

The S&P 500 index is up 7.3% in the trailing six-month period and up 18.4% in the past year.

The stock is currently trading at 11.01X forward 12-month earnings, which compares with 11.01X for the Zacks sub-industry, 16.04X for the Zacks sector and 19.17X for the S&P 500 index.

Over the past five years, the stock has traded as high as 32.36X and as low as 10.81X, with a 5-year median of 15.4X.

Our Neutral recommendation indicates that the stock will perform in-line with the market. Our $380 price target reflects 13.70X our 2023 earnings estimate.

The table below shows summary valuation data for DE.

Industry Analysis(1)Zacks Industry Rank: Bottom 13% (212 out of 245)

Top Peers(1)

| Company (Ticker) | Rec | Rank |

| AGCO Corporation (AGCO) | Outperform | |

| Alamo Group, Inc. (ALG) | Neutral | |

| Caterpillar Inc. (CAT) | Neutral | |

| Ingersoll Rand Inc. (IR) | Neutral | |

| Kubota Corp. (KUBTY) | Neutral | |

| Lindsay Corporation (LNN) | Neutral | |

| Titan International, Inc. (TWI) | NA | NA |

| Astec Industries, Inc. (ASTE) | NA | NA |

Industry Comparison(1)Industry: Manufacturing - Farm Equipment |

Industry Peers |

| DE | |

|---|---|

| Zacks Recommendation (Long Term) | Neutral |

| Zacks Rank (Short Term) | |

| VGM Score | |

| Market Cap | 129.63 B |

| # of Analysts | 12 |

| Dividend Yield | 1.35% |

| Value Score | |

| Cash/Price | 0.07 |

| EV/EBITDA | 11.18 |

| PEG Ratio | -1.98 |

| Price/Book (P/B) | 5.15 |

| Price/Cash Flow (P/CF) | 14.10 |

| P/E (F1) | 17.26 |

| Price/Sales (P/S) | 2.92 |

| Earnings Yield | 3.89% |

| Debt/Equity | 1.76 |

| Cash Flow ($/share) | 33.94 |

| Growth Score | |

| Hist. EPS Growth (3-5 yrs) | 18.29% |

| Proj. EPS Growth (F1/F0) | -19.92% |

| Curr. Cash Flow Growth | -24.26% |

| Hist. Cash Flow Growth (3-5 yrs) | 12.11% |

| Current Ratio | 2.19 |

| Debt/Capital | 63.87% |

| Net Margin | 11.72% |

| Return on Equity | 21.97% |

| Sales/Assets | 0.42 |

| Proj. Sales Growth (F1/F0) | -12.90% |

| Momentum Score | |

| Daily Price Chg | -2.60% |

| 1 Week Price Chg | 1.47% |

| 4 Week Price Chg | -8.72% |

| 12 Week Price Chg | -6.29% |

| 52 Week Price Chg | 25.36% |

| 20 Day Average Volume | 1,456,507 |

| (F1) EPS Est 1 week change | 0.00% |

| (F1) EPS Est 4 week change | -1.15% |

| (F1) EPS Est 12 week change | -1.05% |

| (Q1) EPS Est Mthly Chg | -6.26% |

| X Industry | S&P 500 |

|---|---|

| - | - |

| - | - |

| - | - |

| 1.49 B | 38.19 B |

| 4 | 22 |

| 0.00% | 1.49% |

| - | - |

| 0.11 | 0.04 |

| 10.84 | 14.32 |

| 2.40 | 2.37 |

| 1.89 | 3.55 |

| 11.58 | 14.91 |

| 19.99 | 19.93 |

| 0.79 | 3.06 |

| 4.97% | 4.99% |

| 0.59 | 0.58 |

| 1.55 | 8.99 |

| - | - |

| 13.70% | 9.13% |

| -31.59% | 7.89% |

| -27.19% | 6.75% |

| 9.83% | 7.23% |

| 2.54 | 1.21 |

| 38.19% | 38.33% |

| 6.69% | 12.37% |

| 9.53% | 17.03% |

| 0.85 | 0.53 |

| -2.14% | 4.97% |

| - | - |

| -1.61% | -0.64% |

| 0.74% | 1.41% |

| -0.05% | 1.91% |

| 2.22% | 8.77% |

| 8.43% | 15.53% |

| 334,261 | 2,620,473 |

| 0.00% | 0.00% |

| -1.89% | 0.14% |

| -1.89% | 0.80% |

| -6.26% | 0.00% |

| AGCO | KUBTY | LNN |

|---|---|---|

| Outperform | Neutral | Neutral |

| 8.07 B | 13.39 B | 1.49 B |

| 8 | 2 | 2 |

| 1.07% | 2.15% | 1.08% |

| 0.09 | 0.15 | 0.14 |

| -1,195.97 | 6.81 | 13.48 |

| 1.73 | 5.72 | NA |

| 1.94 | 0.73 | 2.82 |

| 9.05 | 5.78 | 18.07 |

| 22.62 | 12.64 | 20.11 |

| 0.79 | 0.69 | 2.20 |

| 4.42% | 7.91% | 4.97% |

| 0.66 | 0.52 | 0.22 |

| 11.95 | 10.04 | 7.59 |

| 4.04% | 2.54% | 13.70% |

| -36.27% | -29.71% | 13.64% |

| -38.62% | -5.81% | -9.82% |

| 7.76% | 3.59% | 22.76% |

| 1.48 | 1.75 | 3.64 |

| 42.34% | 34.03% | 17.84% |

| 0.98% | 5.97% | 11.21% |

| 8.27% | 6.50% | 15.09% |

| 0.84 | 0.50 | 0.85 |

| -15.80% | -3.70% | 11.00% |

| -4.38% | -3.03% | -1.56% |

| 4.01% | -1.11% | 3.32% |

| -8.29% | 3.46% | 0.53% |

| 7.34% | 4.09% | 1.45% |

| 19.63% | -17.70% | 11.23% |

| 746,543 | 14,720 | 78,563 |

| 0.00% | -8.75% | 0.00% |

| 13.75% | -8.75% | 0.00% |

| 15.78% | -25.49% | 3.96% |

| 8.05% | NA | 0.00% |

Analyst Earnings Model(2)

Zacks Stock Rating System

We offer two rating systems that take into account investors' holding horizons: Zacks Rank and Zacks Recommendation. Each provides valuable insights into the future profitability of the stock and can be used separately or in combination with each other depending on your investment style.

Zacks Recommendation

The Zacks Recommendation aims to predict performance over the next 6 to 12 months. The foundation for the quantitatively determined Zacks Recommendation is trends in the company's estimate revisions and earnings outlook. The Zacks Recommendation is broken down into 3 Levels; Outperform, Neutral and Underperform. Unlike many Wall Street firms, we have an excellent balance between the number of Outperform and Neutral recommendations. Our team of 70 analysts are fully versed in the benefits of earnings estimate revisions and how that is harnessed through the Zacks quantitative rating system. But we have given our analysts the ability to override the Zacks Recommendation for the 1200 stocks that they follow. The reason for the analyst over-rides is that there are often factors such as valuation, industry conditions and management effectiveness that a trained investment professional can spot better than a quantitative model.

Zacks Rank

The Zacks Rank is our short-term rating system that is most effective over the one- to three-month holding horizon. The underlying driver for the quantitatively-determined Zacks Rank is the same as the Zacks Recommendation, and reflects trends in earnings estimate revisions.

Zacks Style Scores

| Value Score |

|

| Growth Score |

|

| Momentum Score |

|

| VGM Score |

|

The Zacks Style Score is as a complementary indicator to the Zacks rating system, giving investors a way to focus on the highest rated stocks that best fit their own stock picking preferences.

Academic research has proven that stocks with the best Value, Growth and Momentum characteristics outperform the market. The Zacks Style Scores rate stocks on each of these individual styles and assigns a rating of A, B, C, D and F. We also produce the VGM Score (V for Value, G for Growth and M for Momentum), which combines the weighted average of the individual Style Scores into one score. This is perfectly suited for those who want their stocks to have the best scores across the board.

As an investor, you want to buy stocks with the highest probability of success. That means buying stocks with a Zacks Recommendation of Outperform, which also has a Style Score of an A or a B.

Disclosures

This report contains independent commentary to be used for informational purposes only. The analysts contributing to this report do not hold any shares of this stock. The analysts contributing to this report do not serve on the board of the company that issued this stock. The EPS and revenue forecasts are the Zacks Consensus estimates, unless otherwise indicated in the report’s first-page footnote. Additionally, the analysts contributing to this report certify that the views expressed herein accurately reflect the analysts' personal views as to the subject securities and issuers. ZIR certifies that no part of the analysts' compensation was, is, or will be, directly or indirectly, related to the specific recommendation or views expressed by the analyst in the report.

Additional information on the securities mentioned in this report is available upon request. This report is based on data obtained from sources we believe to be reliable, but is not guaranteed as to accuracy and does not purport to be complete. Any opinions expressed herein are subject to change.

ZIR is not an investment advisor and the report should not be construed as advice designed to meet the particular investment needs of any investor. Prior to making any investment decision, you are advised to consult with your broker, investment advisor, or other appropriate tax or financial professional to determine the suitability of any investment. This report and others like it are published regularly and not in response to episodic market activity or events affecting the securities industry.

This report is not to be construed as an offer or the solicitation of an offer to buy or sell the securities herein mentioned. ZIR or its officers, employees or customers may have a position long or short in the securities mentioned and buy or sell the securities from time to time. ZIR is not a broker-dealer. ZIR may enter into arms-length agreements with broker-dealers to provide this research to their clients. Zacks and its staff are not involved in investment banking activities for the stock issuer covered in this report.

ZIR uses the following rating system for the securities it covers. Outperform- ZIR expects that the subject company will outperform the broader U.S. equities markets over the next six to twelve months. Neutral- ZIR expects that the company will perform in line with the broader U.S. equities markets over the next six to twelve months. Underperform- ZIR expects the company will underperform the broader U.S. equities markets over the next six to twelve months.

No part of this report can be reprinted, republished or transmitted electronically without the prior written authorization of ZIR.