Block , formerly Square, has endured a challenging two years as the stock has cratered nearly -70% from its late-2021 high. Although the selloff was a major talking point among Wall Street analysts and traders for some time, the stock has seemingly fallen out of the spotlight.

For discerning investors, this is exactly what you want to see.

People have stopped talking about Block, since the stock has been left behind during the incredible tech rally of the last year. But there are a number of bullish catalysts forming in favor of the beaten down payment processor.

Read ahead and see why Block may be the next big addition to your portfolio.

Image Source: TradingView

Earnings Estimates Jump

When a stock falls as precipitously as Block, and investors stop considering it for their portfolio’s you would expect sales and earnings to be falling as well. However, that is not the case.

Block is forecast to grow sales 13% YoY this year and 11.5% next year, while earnings are expected to climb 64% and 31% respectively.

Furthermore, analysts have just begun to take notice and in the chart below we can see that the earnings revision trend has snapped higher in recent weeks.

Block now enjoys a Zacks Rank #1 (Strong Buy) rating, improving the near-term expectations of the stock’s performance.

Image Source: Zacks Investment Research

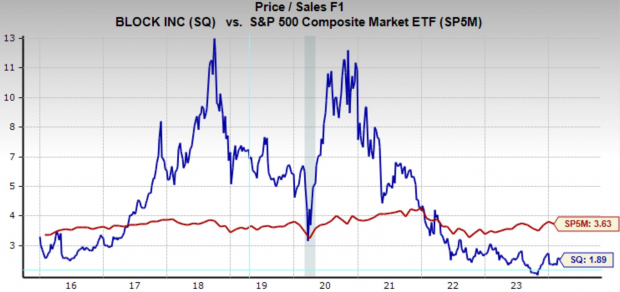

Deep Historical Discount

Block is also trading at a significant historical discount. For a long time, it was one of these hyper growth, buy at any price stocks, which pushed its valuation to lofty and probably unreasonable levels.

Today, SQ is trading at a one year forward sales multiple of 1.9x, below the broad market average and well below its eight-year median of 5x.

Additionally, because the company is now earning considerable profits annually, it can be measured by its forward earnings multiple, which is now just 19.6x based on next year’s EPS forecast of $3.87 per share.

Block is projected to grow its EPS by an incredible 28.1% annually over the next 3-5 years, giving it a PEG ratio of 0.7, indicating a discount valuation based on the metric.

Image Source: Zacks Investment Research

Technical Picture

Finally, Block is on the verge of a prototypical stage one breakout, which if it completes may signal considerable upside moving forward. If the stock can trade above the $80 level, it could mark the beginning of a major bull run.

Image Source: TradingView

Bottom Line

The setup building in Block is in my opinion as straightforward as they get. Sure, payment processors are battling in one of the most competitive industries in the market today, with many of the technology giants today duking it out. But the growth projections speak for themselves.

Block also has a diversified approach in the payment processing market, as they have a peer-to-peer product in Cash App, a brick-and-mortar product, and are a gateway into the crypto world among others.

For investors looking for a contrarian, deep value, technology play, Block is a worthy consideration.

Image: Bigstock

Hidden Gem: Top-Ranked Payment Processor Poised for a Major Breakout

Block , formerly Square, has endured a challenging two years as the stock has cratered nearly -70% from its late-2021 high. Although the selloff was a major talking point among Wall Street analysts and traders for some time, the stock has seemingly fallen out of the spotlight.

For discerning investors, this is exactly what you want to see.

People have stopped talking about Block, since the stock has been left behind during the incredible tech rally of the last year. But there are a number of bullish catalysts forming in favor of the beaten down payment processor.

Read ahead and see why Block may be the next big addition to your portfolio.

Image Source: TradingView

Earnings Estimates Jump

When a stock falls as precipitously as Block, and investors stop considering it for their portfolio’s you would expect sales and earnings to be falling as well. However, that is not the case.

Block is forecast to grow sales 13% YoY this year and 11.5% next year, while earnings are expected to climb 64% and 31% respectively.

Furthermore, analysts have just begun to take notice and in the chart below we can see that the earnings revision trend has snapped higher in recent weeks.

Block now enjoys a Zacks Rank #1 (Strong Buy) rating, improving the near-term expectations of the stock’s performance.

Image Source: Zacks Investment Research

Deep Historical Discount

Block is also trading at a significant historical discount. For a long time, it was one of these hyper growth, buy at any price stocks, which pushed its valuation to lofty and probably unreasonable levels.

Today, SQ is trading at a one year forward sales multiple of 1.9x, below the broad market average and well below its eight-year median of 5x.

Additionally, because the company is now earning considerable profits annually, it can be measured by its forward earnings multiple, which is now just 19.6x based on next year’s EPS forecast of $3.87 per share.

Block is projected to grow its EPS by an incredible 28.1% annually over the next 3-5 years, giving it a PEG ratio of 0.7, indicating a discount valuation based on the metric.

Image Source: Zacks Investment Research

Technical Picture

Finally, Block is on the verge of a prototypical stage one breakout, which if it completes may signal considerable upside moving forward. If the stock can trade above the $80 level, it could mark the beginning of a major bull run.

Image Source: TradingView

Bottom Line

The setup building in Block is in my opinion as straightforward as they get. Sure, payment processors are battling in one of the most competitive industries in the market today, with many of the technology giants today duking it out. But the growth projections speak for themselves.

Block also has a diversified approach in the payment processing market, as they have a peer-to-peer product in Cash App, a brick-and-mortar product, and are a gateway into the crypto world among others.

For investors looking for a contrarian, deep value, technology play, Block is a worthy consideration.