Image Source: Zacks Investment Research

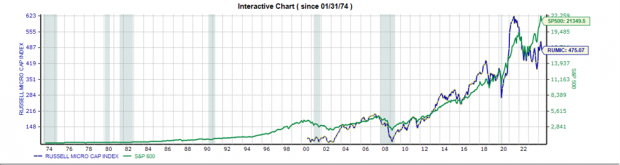

The graph above depicts a rather stark divergence in performance between the S&P 500 and the Russell Microcap Index (RUMIC) over the last 18 months. The S&P 500 is currently trading at a trailing twelve-month PE of approximately 25x vs. 13.3x (excludes negative EPS companies) for the Russell Microcap index. The Magnificent 7 and other growthier tech names have no doubt contributed to the S&P performance. But has an elevated interest rate environment held back microcaps?

Historically, investor perception has been that smaller companies are more burdened by rising interest rates. Small companies typically have floating rate debt that is more sensitive to interest rate fluctuations. Conversely, large companies normally have better lending terms because of their financial size, more proven operating history, and asset quality which affords comforting downside protection to lenders.

Image Source: Zacks Investment Research

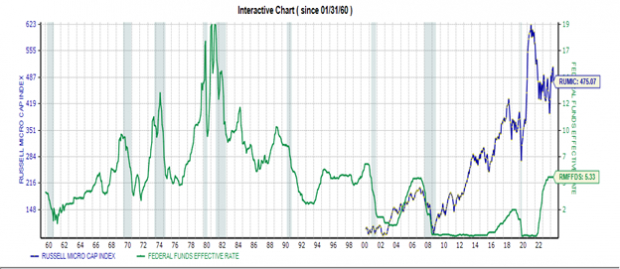

The graph above charts the Federal Feds rate against the performance of the Russell Microcap Index, which was launched in 2005. Keep in mind that this dataset is somewhat limited in that it only covers about 20 years with only two major economic events, the GFC (Great Financial Crisis) and the Covid pandemic.

Clearly, microcaps performed very well during the near zero rate period. But equities were the only game in town as yield was scarce everywhere else, so the risk-on trade was especially strong.

But during the slower paced raising period of 2016-2019 microcaps continued to rise, showing resilience to the rising rates, albeit from a very low base. So even though rates went from near zero to 2%, risk-free alternatives were still not very compelling and the risk-on trade prevailed.

Microcaps briefly retreated significantly due to Covid but then rebounded as interest rates again retreated near zero during the post-Covid recovery. But the “accelerated” climb in rates from 0 to 5% did not go well for microcaps. A 5% risk-free return is very compelling, especially to investors who haven’t seen that level of rates in 17 years and especially relative to the inherent volatility of microcaps.

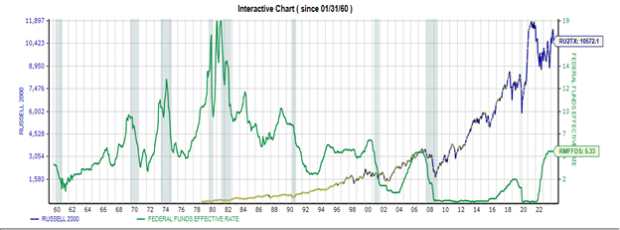

We can elongate the data back to 1984 by using the Russell 2000 index as a proxy for small companies. This index has “bigger” small companies than the Russell Microcap index and was launched in 1984. As of 4/30/24 the average market cap in the index was $4.3B with a median market cap of $879 m vs. $859 m and $213 m, respectively, for the Russell Microcap. This index is frequently used as a benchmark for small cap performance.

Image Source: Zacks Investment Research

The graph above charts the Russell 2000 performance against the Federal Funds Rate. Going back to 1984 yields additional data points to consider including a few additional recessions as well as more tightening and loosening periods. Interestingly, small caps showed less positive reaction to the lowering of rates from 10% to 3% to thwart the 1990 recession vs. the lowering of rates from near 7% to 1% to counter the 2000/2001 recession.

So “when” the Fed begins cutting rates, could Microcaps potentially recover and shine again? Will the risk-on trade for Microcaps return? There is some recent evidence that suggests that the market thinks so.

For instance, on November 14th when a positive inflation print posted, and thus implicitly the prospect of rate loosening, the Russell Microcap index rose 5.4%. Additionally, when Fed commentary on December 13th suggested three possible rate cuts in 2024, the Russell Microcap index responded with gains of 3.8% on 12/13 and 2.3% on 12/14. This is also reflective of the larger and ongoing discussion about the forces driving stock market performance-macro economy vs. interest rates.

Such positive and arguably hyper-sensitive responses have led some to believe that micro caps are a “tightly coiled spring”, ready to unleash if a steady path of lowering rates begin. We believe this could occur but rate declines would need to be consistent and prolonged in order to materially bring down the risk-free alternative rate.

The market is currently pricing in about a 2.4% Fed Funds rate by the end of 2026 which we believe could be sufficient to move the needle of asset class momentum assuming it comes to fruition. But inflation is proving sticker than expected and this potential cadence of interest rate declines may not materialize as envisioned. In fact, the Fed Funds Futures have a poor track record of predicting the timing of rate changes. Regardless, it is a real time market barometer of what the market is thinking, a “put your money where your mouth is” litmus test.

As mentioned previously, microcaps tend to have floating rate debt so declines in interest rates would pretty quickly result in declines in interest rate expenses and could materially improve Earnings Per Share for debt laden companies. These interest rate declines would also probably need to be accompanied by a stable economy in order for microcaps outperformance to accrue. As the graphs above demonstrated, microcaps responded violently downward to economic crises.

Perhaps most importantly, the Fed Funds rate dictates the cost of capital, and consequently, the discount rate for calculating the present value of future cash flows. Due to the power of math and compounding over future periods, declines in rates will have an outsized impact on current DCF (discounted cash flow) valuations. So, declines in interest rates could make microcaps especially more compelling on a valuation front before the market prices catch up, and thus represent a buying opportunity.

Independent of the impact of interest rates, investors need to be aware of the unique properties of microcaps. For instance, microcap companies tend to have less international exposure as the majority of their sales and costs are US based. Thus, they tend to be more insulated from geopolitical risks including tariff issues and US dollar strength/weakness.

Microcaps also benefitted disproportionately from corporate tax reform (35% to 21%) as larger companies tend to operate in foreign tax jurisdictions with comparatively lower tax rates which reduces their overall tax rate. So, any future legislation related to trade or tax policy is especially relevant for microcaps especially relative to large caps.

Microcap stocks, with their domestic focus, could also benefit from the onshoring phenomenon of bringing manufacturing back to the US as well as large-scale US fiscal spending on infrastructure.

In conclusion, microcaps presently look undervalued at these levels, especially relative to their large cap brethren. There are also several positive conditions which could uniquely benefit the financial performance of microcaps. And the market perception of their sensitivity to interest rates appears alive and well.

But we still maintain a stable economy is required to work in concert with possible rate reductions to enable possible microcap outperformance. And the timing and cadence of such possible rate reductions remains uncertain, driven by the forces of inflation and the strength of the overall economy.

As an investment strategy one could buy the Russell Microcap ETF for microcap exposure but investors should be aware that as of 4/30/24 the index skewed 25.5% towards healthcare (including biotech) and 19.1% financials. Volatility in these two sectors can materially impact the performance of the index. Additionally, investors should be aware that there are many unprofitable companies in the index as well.

Or, one could buy a basket of microcap stocks rated Outperform by the Zacks Microcap team. The Zacks rating system utilizes both quantitative and qualitative methods to “control for junk.” It acts as a filter to remove the impurities inherent in the index.

Academic research has shown that “controlling for junk” is necessary to validate the “size effect” inherent in microcaps which has led to long term outperformance, but with significant volatility. See our previous discussion about the “size effect” here.

The Zacks screening process factors in macro-economic sensitivity and interest rate sensitivity at the individual company level. Some current Outperform recommendations by Zacks include INOD, HFFG, CSPI, FEIM, and GENC.

INOD (Innodata Inc.) is a “picks and shovels” play on AI. Innodata provides data testing services for companies developing AI products. They have landed contracts with several of the major tech players and stand poised to benefit from elevated investment spending in AI.

HFFG (HF Foods Group Inc.) is a distributor to the highly fragmented and consistently growing Asian restaurant industry in the US. The industry lacks the purchasing power of large chain restaurants and thus relies heavily upon distribution. HF Foods Groups focuses on especially time-sensitive food staples like seafood and produce.

CSPI (CSP Inc.) is a reseller of computer hardware and software across multiple industry verticals. But CSP's higher margin cybersecurity software product ARIA has been gaining traction and addresses the growing incidence of cyber attacks against critical infrastructure (e.g. utilities) in the US.

FEIM (Frequency Electronics, Inc) is a designer and manufacturer of precision time and frequency control components for both land-based communication systems and satellites. Frequency Electronics should benefit from elevated global defense spending.

GENC (Gencor Industries, Inc.) designs and manufactures heavy machinery used in the production of highway construction materials like asphalt and environmental control equipment. Gencor Industries should continue to benefit from US infrastructure spending.

Image: Bigstock

Are Microcaps Setting Up to Outperform?

Image Source: Zacks Investment Research

The graph above depicts a rather stark divergence in performance between the S&P 500 and the Russell Microcap Index (RUMIC) over the last 18 months. The S&P 500 is currently trading at a trailing twelve-month PE of approximately 25x vs. 13.3x (excludes negative EPS companies) for the Russell Microcap index. The Magnificent 7 and other growthier tech names have no doubt contributed to the S&P performance. But has an elevated interest rate environment held back microcaps?

Historically, investor perception has been that smaller companies are more burdened by rising interest rates. Small companies typically have floating rate debt that is more sensitive to interest rate fluctuations. Conversely, large companies normally have better lending terms because of their financial size, more proven operating history, and asset quality which affords comforting downside protection to lenders.

Image Source: Zacks Investment Research

The graph above charts the Federal Feds rate against the performance of the Russell Microcap Index, which was launched in 2005. Keep in mind that this dataset is somewhat limited in that it only covers about 20 years with only two major economic events, the GFC (Great Financial Crisis) and the Covid pandemic.

Clearly, microcaps performed very well during the near zero rate period. But equities were the only game in town as yield was scarce everywhere else, so the risk-on trade was especially strong.

But during the slower paced raising period of 2016-2019 microcaps continued to rise, showing resilience to the rising rates, albeit from a very low base. So even though rates went from near zero to 2%, risk-free alternatives were still not very compelling and the risk-on trade prevailed.

Microcaps briefly retreated significantly due to Covid but then rebounded as interest rates again retreated near zero during the post-Covid recovery. But the “accelerated” climb in rates from 0 to 5% did not go well for microcaps. A 5% risk-free return is very compelling, especially to investors who haven’t seen that level of rates in 17 years and especially relative to the inherent volatility of microcaps.

We can elongate the data back to 1984 by using the Russell 2000 index as a proxy for small companies. This index has “bigger” small companies than the Russell Microcap index and was launched in 1984. As of 4/30/24 the average market cap in the index was $4.3B with a median market cap of $879 m vs. $859 m and $213 m, respectively, for the Russell Microcap. This index is frequently used as a benchmark for small cap performance.

Image Source: Zacks Investment Research

The graph above charts the Russell 2000 performance against the Federal Funds Rate. Going back to 1984 yields additional data points to consider including a few additional recessions as well as more tightening and loosening periods. Interestingly, small caps showed less positive reaction to the lowering of rates from 10% to 3% to thwart the 1990 recession vs. the lowering of rates from near 7% to 1% to counter the 2000/2001 recession.

So “when” the Fed begins cutting rates, could Microcaps potentially recover and shine again? Will the risk-on trade for Microcaps return? There is some recent evidence that suggests that the market thinks so.

For instance, on November 14th when a positive inflation print posted, and thus implicitly the prospect of rate loosening, the Russell Microcap index rose 5.4%. Additionally, when Fed commentary on December 13th suggested three possible rate cuts in 2024, the Russell Microcap index responded with gains of 3.8% on 12/13 and 2.3% on 12/14. This is also reflective of the larger and ongoing discussion about the forces driving stock market performance-macro economy vs. interest rates.

Such positive and arguably hyper-sensitive responses have led some to believe that micro caps are a “tightly coiled spring”, ready to unleash if a steady path of lowering rates begin. We believe this could occur but rate declines would need to be consistent and prolonged in order to materially bring down the risk-free alternative rate.

The market is currently pricing in about a 2.4% Fed Funds rate by the end of 2026 which we believe could be sufficient to move the needle of asset class momentum assuming it comes to fruition. But inflation is proving sticker than expected and this potential cadence of interest rate declines may not materialize as envisioned. In fact, the Fed Funds Futures have a poor track record of predicting the timing of rate changes. Regardless, it is a real time market barometer of what the market is thinking, a “put your money where your mouth is” litmus test.

As mentioned previously, microcaps tend to have floating rate debt so declines in interest rates would pretty quickly result in declines in interest rate expenses and could materially improve Earnings Per Share for debt laden companies. These interest rate declines would also probably need to be accompanied by a stable economy in order for microcaps outperformance to accrue. As the graphs above demonstrated, microcaps responded violently downward to economic crises.

Perhaps most importantly, the Fed Funds rate dictates the cost of capital, and consequently, the discount rate for calculating the present value of future cash flows. Due to the power of math and compounding over future periods, declines in rates will have an outsized impact on current DCF (discounted cash flow) valuations. So, declines in interest rates could make microcaps especially more compelling on a valuation front before the market prices catch up, and thus represent a buying opportunity.

Independent of the impact of interest rates, investors need to be aware of the unique properties of microcaps. For instance, microcap companies tend to have less international exposure as the majority of their sales and costs are US based. Thus, they tend to be more insulated from geopolitical risks including tariff issues and US dollar strength/weakness.

Microcaps also benefitted disproportionately from corporate tax reform (35% to 21%) as larger companies tend to operate in foreign tax jurisdictions with comparatively lower tax rates which reduces their overall tax rate. So, any future legislation related to trade or tax policy is especially relevant for microcaps especially relative to large caps.

Microcap stocks, with their domestic focus, could also benefit from the onshoring phenomenon of bringing manufacturing back to the US as well as large-scale US fiscal spending on infrastructure.

In conclusion, microcaps presently look undervalued at these levels, especially relative to their large cap brethren. There are also several positive conditions which could uniquely benefit the financial performance of microcaps. And the market perception of their sensitivity to interest rates appears alive and well.

But we still maintain a stable economy is required to work in concert with possible rate reductions to enable possible microcap outperformance. And the timing and cadence of such possible rate reductions remains uncertain, driven by the forces of inflation and the strength of the overall economy.

As an investment strategy one could buy the Russell Microcap ETF for microcap exposure but investors should be aware that as of 4/30/24 the index skewed 25.5% towards healthcare (including biotech) and 19.1% financials. Volatility in these two sectors can materially impact the performance of the index. Additionally, investors should be aware that there are many unprofitable companies in the index as well.

Or, one could buy a basket of microcap stocks rated Outperform by the Zacks Microcap team. The Zacks rating system utilizes both quantitative and qualitative methods to “control for junk.” It acts as a filter to remove the impurities inherent in the index.

Academic research has shown that “controlling for junk” is necessary to validate the “size effect” inherent in microcaps which has led to long term outperformance, but with significant volatility. See our previous discussion about the “size effect” here.

The Zacks screening process factors in macro-economic sensitivity and interest rate sensitivity at the individual company level. Some current Outperform recommendations by Zacks include INOD, HFFG, CSPI, FEIM, and GENC.

INOD (Innodata Inc.) is a “picks and shovels” play on AI. Innodata provides data testing services for companies developing AI products. They have landed contracts with several of the major tech players and stand poised to benefit from elevated investment spending in AI.

HFFG (HF Foods Group Inc.) is a distributor to the highly fragmented and consistently growing Asian restaurant industry in the US. The industry lacks the purchasing power of large chain restaurants and thus relies heavily upon distribution. HF Foods Groups focuses on especially time-sensitive food staples like seafood and produce.

CSPI (CSP Inc.) is a reseller of computer hardware and software across multiple industry verticals. But CSP's higher margin cybersecurity software product ARIA has been gaining traction and addresses the growing incidence of cyber attacks against critical infrastructure (e.g. utilities) in the US.

FEIM (Frequency Electronics, Inc) is a designer and manufacturer of precision time and frequency control components for both land-based communication systems and satellites. Frequency Electronics should benefit from elevated global defense spending.

GENC (Gencor Industries, Inc.) designs and manufactures heavy machinery used in the production of highway construction materials like asphalt and environmental control equipment. Gencor Industries should continue to benefit from US infrastructure spending.