Disappointing results for A-Mark Precious Metals' fiscal second quarter makes its stock one to avoid after releasing its Q2 report last Friday.

Operating as a full-service precious metals trading company, A-Mark has been vulnerable to a weaker business environment with reduced demand and higher operating costs impacting its profitability. Considering such, AMRK lands a Zacks Rank #5 (Strong Sell) and the Bear of the Day.

A-Mark’s Disappointing Q2 Results

A-Mark's Q2 EPS of $0.55 dropped from $0.90 per share in the comparative quarter and missed expectations of $0.86 by -36%. This was despite Q2 sales of $2.74 billion rising from $2.07 billion in the prior period and edging estimates of $2.66 billion.

Still, the company’s operating efficiency has to be called into question as A-Mark has missed earnings expectations for six consecutive quarters with an average EPS surprise of -42.03% in its last four quarterly reports.

Image Source: Zacks Investment Research

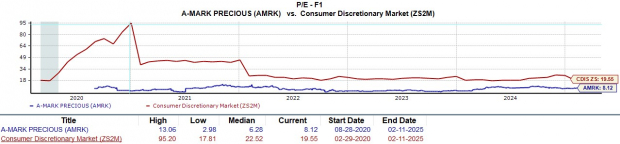

A-Marks Misleading Valuation

A-Mark's stock could be a value trap for investors who aren’t keeping up with the company’s financial performance and blindly rely on its valuation with AMRK at a “cheap” 8.1X forward earnings multiple.

Image Source: Zacks Investment Research

Taking away from A-Mark's P/E discount relative to the consumer discretionary sector is that its fiscal 2025 EPS estimates have noticeably declined over the last seven months after dropping 20% in the last week to $2.83 from $3.54.

Image Source: Zacks Investment Research

Bottom Line

Harvesting gold, silver, and platinum, A-Mark’s operations may be appealing down the line but for now, it may be best to avoid AMRK. To that point, A-Mark needs to show it can get back on track in regards to reaching its earnings potential as declining EPS estimates point to more downside risk ahead.

Bear of the Day: AMark Precious Metals (AMRK)

Disappointing results for A-Mark Precious Metals' fiscal second quarter makes its stock one to avoid after releasing its Q2 report last Friday.

Operating as a full-service precious metals trading company, A-Mark has been vulnerable to a weaker business environment with reduced demand and higher operating costs impacting its profitability. Considering such, AMRK lands a Zacks Rank #5 (Strong Sell) and the Bear of the Day.

A-Mark’s Disappointing Q2 Results

A-Mark's Q2 EPS of $0.55 dropped from $0.90 per share in the comparative quarter and missed expectations of $0.86 by -36%. This was despite Q2 sales of $2.74 billion rising from $2.07 billion in the prior period and edging estimates of $2.66 billion.

Still, the company’s operating efficiency has to be called into question as A-Mark has missed earnings expectations for six consecutive quarters with an average EPS surprise of -42.03% in its last four quarterly reports.

Image Source: Zacks Investment Research

A-Marks Misleading Valuation

A-Mark's stock could be a value trap for investors who aren’t keeping up with the company’s financial performance and blindly rely on its valuation with AMRK at a “cheap” 8.1X forward earnings multiple.

Image Source: Zacks Investment Research

Taking away from A-Mark's P/E discount relative to the consumer discretionary sector is that its fiscal 2025 EPS estimates have noticeably declined over the last seven months after dropping 20% in the last week to $2.83 from $3.54.

Image Source: Zacks Investment Research

Bottom Line

Harvesting gold, silver, and platinum, A-Mark’s operations may be appealing down the line but for now, it may be best to avoid AMRK. To that point, A-Mark needs to show it can get back on track in regards to reaching its earnings potential as declining EPS estimates point to more downside risk ahead.