The Zacks Business Services sector has tumbled in 2022, down more than 25% and widely underperforming the S&P 500.

A widely-recognized name in the realm, Block , is on deck to unveil Q3 earnings on November 3rd, after the market close.

Block offers financial and marketing services through its comprehensive commerce ecosystem that helps sellers to start, run and grow their businesses.

Currently, the company carries a Zacks Rank #4 (Sell) paired with an overall VGM Score of a D.

How does everything else stack up for the company? Let’s take a deeper dive.

Share Performance & Valuation

It’s been a challenging road for SQ shares in 2022, down more than 60% and coming nowhere near the general market’s performance.

Image Source: Zacks Investment Research

Over the last three months, the adverse price action of SQ shares has continued, down more than 30% and again lagging the S&P 500.

Image Source: Zacks Investment Research

The company’s valuation multiples have pulled back amid the stretch of poor price action; its forward price-to-sales ratio of 1.9X is nowhere near its 6.5X five-year median and is a fraction of 2021 highs of 9.4X.

Further, the value represents a 72% discount relative to its Zacks Business Services sector average.

Image Source: Zacks Investment Research

Quarterly Estimates

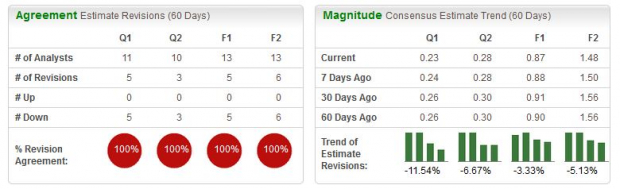

Analysts have been bearish in their earnings outlook, with five negative earnings estimate revisions coming in over the last several months. The Zacks Consensus EPS Estimate of $0.23 indicates a Y/Y decline in earnings of roughly 37%.

Image Source: Zacks Investment Research

SQ’s top-line is in better health; the Zacks Consensus Sales Estimate of $4.5 billion indicates a Y/Y improvement of roughly 16%.

Quarterly Performance & Market Reactions

Block has primarily exceeded earnings expectations, penciling in seven EPS beats across its last ten quarters. In its latest release, the company reported earnings in line with expectations.

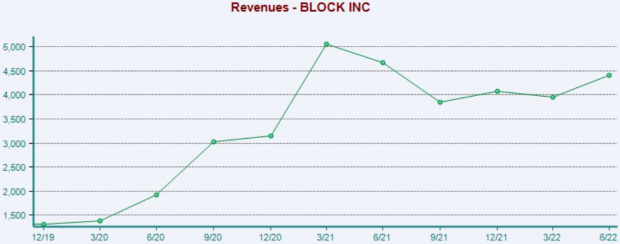

Revenue results have been mixed; SQ has exceeded sales expectations twice across its last four quarters. Below is a chart illustrating the company’s revenue on a quarterly basis.

Image Source: Zacks Investment Research

Additionally, it’s worth noting that shares have moved downward following its latest two prints, indicating that the market hasn’t been impressed with the results.

Putting Everything Together

SQ shares have fallen notably in 2022, underperforming the general market across several timeframes.

The company’s forward price-to-sales ratio is nowhere near its historical values, sitting well beneath its Zacks Business Services sector average.

Analysts have pulled back their earnings expectations over the last several months, with estimates suggesting a Y/Y decline in earnings but an uptick in revenue, likely a reflection of rising costs eating into margins.

The company has primarily exceeded bottom-line estimates, but revenue results have been a mixed bag across its last four releases.

Heading into the print, Block carries a Zacks Rank #4 (Sell) with an Earnings ESP Score of 3%.

Image: Shutterstock

Block Q3 Preview: Can Shares Find New Life?

The Zacks Business Services sector has tumbled in 2022, down more than 25% and widely underperforming the S&P 500.

A widely-recognized name in the realm, Block , is on deck to unveil Q3 earnings on November 3rd, after the market close.

Block offers financial and marketing services through its comprehensive commerce ecosystem that helps sellers to start, run and grow their businesses.

Currently, the company carries a Zacks Rank #4 (Sell) paired with an overall VGM Score of a D.

How does everything else stack up for the company? Let’s take a deeper dive.

Share Performance & Valuation

It’s been a challenging road for SQ shares in 2022, down more than 60% and coming nowhere near the general market’s performance.

Image Source: Zacks Investment Research

Over the last three months, the adverse price action of SQ shares has continued, down more than 30% and again lagging the S&P 500.

Image Source: Zacks Investment Research

The company’s valuation multiples have pulled back amid the stretch of poor price action; its forward price-to-sales ratio of 1.9X is nowhere near its 6.5X five-year median and is a fraction of 2021 highs of 9.4X.

Further, the value represents a 72% discount relative to its Zacks Business Services sector average.

Image Source: Zacks Investment Research

Quarterly Estimates

Analysts have been bearish in their earnings outlook, with five negative earnings estimate revisions coming in over the last several months. The Zacks Consensus EPS Estimate of $0.23 indicates a Y/Y decline in earnings of roughly 37%.

Image Source: Zacks Investment Research

SQ’s top-line is in better health; the Zacks Consensus Sales Estimate of $4.5 billion indicates a Y/Y improvement of roughly 16%.

Quarterly Performance & Market Reactions

Block has primarily exceeded earnings expectations, penciling in seven EPS beats across its last ten quarters. In its latest release, the company reported earnings in line with expectations.

Revenue results have been mixed; SQ has exceeded sales expectations twice across its last four quarters. Below is a chart illustrating the company’s revenue on a quarterly basis.

Image Source: Zacks Investment Research

Additionally, it’s worth noting that shares have moved downward following its latest two prints, indicating that the market hasn’t been impressed with the results.

Putting Everything Together

SQ shares have fallen notably in 2022, underperforming the general market across several timeframes.

The company’s forward price-to-sales ratio is nowhere near its historical values, sitting well beneath its Zacks Business Services sector average.

Analysts have pulled back their earnings expectations over the last several months, with estimates suggesting a Y/Y decline in earnings but an uptick in revenue, likely a reflection of rising costs eating into margins.

The company has primarily exceeded bottom-line estimates, but revenue results have been a mixed bag across its last four releases.

Heading into the print, Block carries a Zacks Rank #4 (Sell) with an Earnings ESP Score of 3%.