We use cookies to understand how you use our site and to improve your experience.

This includes personalizing content and advertising.

By pressing "Accept All" or closing out of this banner, you consent to the use of all cookies and similar technologies and the sharing of information they collect with third parties.

You can reject marketing cookies by pressing "Deny Optional," but we still use essential, performance, and functional cookies.

In addition, whether you "Accept All," Deny Optional," click the X or otherwise continue to use the site, you accept our Privacy Policy and Terms of Service, revised from time to time.

You are being directed to ZacksTrade, a division of LBMZ Securities and licensed broker-dealer. ZacksTrade and Zacks.com are separate companies. The web link between the two companies is not a solicitation or offer to invest in a particular security or type of security. ZacksTrade does not endorse or adopt any particular investment strategy, any analyst opinion/rating/report or any approach to evaluating individual securities.

If you wish to go to ZacksTrade, click OK. If you do not, click Cancel.

LendingTree (TREE) Rides on Growth Efforts Amid Weak Liquidity

Read MoreHide Full Article

LendingTree, Inc.’s (TREE - Free Report) continuous efforts to diversify non-mortgage product offerings and focus on the Consumer segment are driving its revenue growth. Strategic acquisitions over the years have also been supporting financials. However, owing to the challenging operating environment, the Insurance segment’s growth is expected to be subdued, while the weak liquidity position will hamper the capital deployment activities.

TREE has three reportable segments namely Home, Consumer and Insurance. The company has been enhancing revenues by diversifying its non-mortgage product offerings, particularly in the Consumer segment. In February 2023, LendingTree launched WinCard, which was its first branded consumer credit offering. Apart from improved credit card offerings, the company has also widened its loan offerings to personal, auto, small business and student loans. Such strategic initiatives, including SPRING (previously MyLendingTree) and TreeQual, are likely to improve cross-selling opportunities, thus, driving profitability.

TREE’s Home segment’s revenues (consisting of Home Equity revenues and mortgage revenues) have seen an upward trend over the years. This is a result of the company’s focus on improving purchase conversion rates, while assisting in meeting its customers’ demands for home equity loans. Additionally, the company’s market-leading position and flexible business model, offering diverse solutions for a wide range of lenders, will help it navigate through fluctuating macroeconomic conditions and high interest rates environment.

Further, the company is focused on growing inorganically. Since 2016, TREE has successfully integrated many buyouts, supporting its bottom-line growth. The firm enhanced its credit services and credit card product offerings as well as strengthened its online lending platform through acquisitions in the past few years. In first-quarter 2022, it acquired EarnUp, a consumer-facing payments platform. Such strategic initiatives will continue to support bottom-line growth in the future.

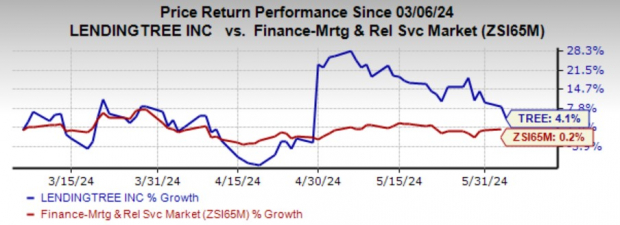

Shares of this Zacks Rank #3 (Hold) company have gained 4.1% compared with its industry’s 0.2% growth over the past six months.

Image Source: Zacks Investment Research

Despite the above-mentioned tailwinds, LendingTree’s Insurance segments revenues have declined over the past few years. Any weakness in personal auto loans and reduced marketing spending by partners will keep the demand subdued.

Although, the company’s cost base has declined in the recent past on the back of cost-containment efforts, the normalization of business activities will likely increase technology and advertisement expenses in the coming months. This might affect bottom-line growth in the long term.

As of Mar 31, 2024, LendingTree’s cash and cash equivalents were $230.7 million, while its long-term debt was significantly higher at $631.3 million. Hence, with the limited cash levels and a higher debt/equity ratio than the industry average, the company’s capital deployment activities seem unsustainable in the near term.

Finance Stocks Worth Considering

Some better-ranked bank stocks worth mentioning are Velocity Financial, Inc. (VEL - Free Report) and Ocwen Financial Corporation .

Velocity Financial’s earnings estimates for 2024 have been revised upward by 8.2% in the past seven days. The company’s shares have gained 29% over the past six months. At present, VEL sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Ocwen Financial’s 2024 earnings estimates have remained unchanged in the past 30 days. The stock has lost 3% over the past three months. Currently, OCN carries a Zacks Rank #2 (Buy).

Zacks' 7 Best Strong Buy Stocks (New Research Report)

Valued at $99, click below to receive our just-released report

predicting the 7 stocks that will soar highest in the coming month.

Image: Bigstock

LendingTree (TREE) Rides on Growth Efforts Amid Weak Liquidity

LendingTree, Inc.’s (TREE - Free Report) continuous efforts to diversify non-mortgage product offerings and focus on the Consumer segment are driving its revenue growth. Strategic acquisitions over the years have also been supporting financials. However, owing to the challenging operating environment, the Insurance segment’s growth is expected to be subdued, while the weak liquidity position will hamper the capital deployment activities.

TREE has three reportable segments namely Home, Consumer and Insurance. The company has been enhancing revenues by diversifying its non-mortgage product offerings, particularly in the Consumer segment. In February 2023, LendingTree launched WinCard, which was its first branded consumer credit offering. Apart from improved credit card offerings, the company has also widened its loan offerings to personal, auto, small business and student loans. Such strategic initiatives, including SPRING (previously MyLendingTree) and TreeQual, are likely to improve cross-selling opportunities, thus, driving profitability.

TREE’s Home segment’s revenues (consisting of Home Equity revenues and mortgage revenues) have seen an upward trend over the years. This is a result of the company’s focus on improving purchase conversion rates, while assisting in meeting its customers’ demands for home equity loans. Additionally, the company’s market-leading position and flexible business model, offering diverse solutions for a wide range of lenders, will help it navigate through fluctuating macroeconomic conditions and high interest rates environment.

Further, the company is focused on growing inorganically. Since 2016, TREE has successfully integrated many buyouts, supporting its bottom-line growth. The firm enhanced its credit services and credit card product offerings as well as strengthened its online lending platform through acquisitions in the past few years. In first-quarter 2022, it acquired EarnUp, a consumer-facing payments platform. Such strategic initiatives will continue to support bottom-line growth in the future.

Shares of this Zacks Rank #3 (Hold) company have gained 4.1% compared with its industry’s 0.2% growth over the past six months.

Image Source: Zacks Investment Research

Despite the above-mentioned tailwinds, LendingTree’s Insurance segments revenues have declined over the past few years. Any weakness in personal auto loans and reduced marketing spending by partners will keep the demand subdued.

Although, the company’s cost base has declined in the recent past on the back of cost-containment efforts, the normalization of business activities will likely increase technology and advertisement expenses in the coming months. This might affect bottom-line growth in the long term.

As of Mar 31, 2024, LendingTree’s cash and cash equivalents were $230.7 million, while its long-term debt was significantly higher at $631.3 million. Hence, with the limited cash levels and a higher debt/equity ratio than the industry average, the company’s capital deployment activities seem unsustainable in the near term.

Finance Stocks Worth Considering

Some better-ranked bank stocks worth mentioning are Velocity Financial, Inc. (VEL - Free Report) and Ocwen Financial Corporation .

Velocity Financial’s earnings estimates for 2024 have been revised upward by 8.2% in the past seven days. The company’s shares have gained 29% over the past six months. At present, VEL sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Ocwen Financial’s 2024 earnings estimates have remained unchanged in the past 30 days. The stock has lost 3% over the past three months. Currently, OCN carries a Zacks Rank #2 (Buy).