We use cookies to understand how you use our site and to improve your experience.

This includes personalizing content and advertising.

By pressing "Accept All" or closing out of this banner, you consent to the use of all cookies and similar technologies and the sharing of information they collect with third parties.

You can reject marketing cookies by pressing "Deny Optional," but we still use essential, performance, and functional cookies.

In addition, whether you "Accept All," Deny Optional," click the X or otherwise continue to use the site, you accept our Privacy Policy and Terms of Service, revised from time to time.

You are being directed to ZacksTrade, a division of LBMZ Securities and licensed broker-dealer. ZacksTrade and Zacks.com are separate companies. The web link between the two companies is not a solicitation or offer to invest in a particular security or type of security. ZacksTrade does not endorse or adopt any particular investment strategy, any analyst opinion/rating/report or any approach to evaluating individual securities.

If you wish to go to ZacksTrade, click OK. If you do not, click Cancel.

Credo's Diversification Push: Can It Cut Customer Concentration Risk?

Read MoreHide Full Article

Key Takeaways

CRDO relies heavily on hyperscalers, with top customers contributing a large share of revenue.

Credo is expanding into Neo clouds, expecting 20% revenue contribution over time.

For CRDO, hyperscalers are likely to remain key, with diversification likely gradual, not immediate.

Credo Technology Group (CRDO - Free Report) has been delivering explosive revenue growth, but customer concentration remains a key concern.

CRDO delivered 157% year-over-year revenue growth for the fourth quarter of fiscal 2026. Four hyperscalers each contributed 10% or more of total revenues in the last reported quarter, with the top three customers representing 34%, 27%, and 16% of revenues. It also has a fifth hyperscaler customer, further strengthening its position within the global cloud ecosystem.

That said, heavy reliance on a few hyperscalers can introduce volatility, particularly given the cyclical nature of AI infrastructure spending.

Image Source: Zacks Investment Research

Credo is actively working to reduce this reliance through a diversification strategy across hyperscalers, neo clouds and other customers. Neo cloud providers are the emerging players in the AI infrastructure space. This particular set of cloud providers is heavily into AI infrastructure building to support a wide range of applications from model development to inference AI and even Agentic AI workloads. This is driving demand for high-speed connectivity solutions, which bodes well for CRDO.

Notably, management believes this segment could become a meaningful contributor over time, potentially reaching around 20% of revenue.

Nonetheless, Credo continues to expect that three to four customers will account for more than 10% of revenues in the upcoming quarters. This suggests that the diversification push will likely be gradual rather than immediate. Though the customer mix is expected to vary quarter to quarter, hyperscaler spending will remain central to revenue growth given their scale.

Overall, Credo’s concentration risk is unlikely to disappear overnight, but the company is clearly moving toward a more balanced customer base, which could meaningfully reduce this risk over time.

Taking a Look at Rivals’ Hyperscaler Ties

Broadcom (AVGO - Free Report) sees massive opportunities in the AI space, as its hyperscaler customers have begun developing their own custom accelerators or XPUs. The company is building custom silicon platforms and enabling massive compute deployments for leading hyperscalers such as Meta, as well as AI companies like Anthropic and OpenAI.

For OpenAI, AVGO has a contractual commitment to deploy 1.3 gigawatts in 2027 as part of the wider 10-gigawatt agreement by 2029. AVGO announced an agreement with Meta in April under which it would deliver multiple generations of MTIA XPUs and deploy 3 gigawatts by 2028. AI semiconductor revenues are expected to reach $16 billion in the third quarter of fiscal 2026, up more than 200% year over year.

Marvell Technology’s (MRVL - Free Report) hyperscaler exposure remains central to its growth strategy. On the last earnings call, management highlighted that it now ships DCI solutions to all five major U.S. hyperscalers. It expects to gain from rising demand, driven by large-scale AI clusters that increasingly span several data centers. This shift is accelerating bandwidth needs and driving adoption of higher-speed interconnect solutions like 800G and 1.6T.

Marvell noted that it is engaged with multiple Tier 1 hyperscalers across emerging areas such as scale-up networks, AECs and XPUs. While hyperscaler traction underscores strong revenue visibility, it also highlights risks stemming from reliance on hyperscaler capex cycles.

CRDO’s Price Performance, Valuation and Estimates

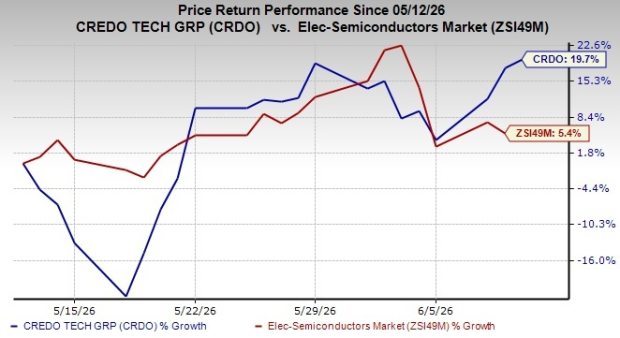

Shares of CRDO have gained 19.7% in the past month, while the Electronics-Semiconductors industry is up 5.4%.

p> Image Source: Zacks Investment Research

In terms of the forward 12-month price/sales ratio, CRDO is trading at 17.71, higher than the Electronic-Semiconductors industry’s multiple of 9.14.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for CRDO’s earnings for fiscal 2027 has been revised upward over the past 60 days.

Image: Bigstock

Credo's Diversification Push: Can It Cut Customer Concentration Risk?

Key Takeaways

Credo Technology Group (CRDO - Free Report) has been delivering explosive revenue growth, but customer concentration remains a key concern.

CRDO delivered 157% year-over-year revenue growth for the fourth quarter of fiscal 2026. Four hyperscalers each contributed 10% or more of total revenues in the last reported quarter, with the top three customers representing 34%, 27%, and 16% of revenues. It also has a fifth hyperscaler customer, further strengthening its position within the global cloud ecosystem.

That said, heavy reliance on a few hyperscalers can introduce volatility, particularly given the cyclical nature of AI infrastructure spending.

Image Source: Zacks Investment Research

Credo is actively working to reduce this reliance through a diversification strategy across hyperscalers, neo clouds and other customers. Neo cloud providers are the emerging players in the AI infrastructure space. This particular set of cloud providers is heavily into AI infrastructure building to support a wide range of applications from model development to inference AI and even Agentic AI workloads. This is driving demand for high-speed connectivity solutions, which bodes well for CRDO.

Notably, management believes this segment could become a meaningful contributor over time, potentially reaching around 20% of revenue.

Nonetheless, Credo continues to expect that three to four customers will account for more than 10% of revenues in the upcoming quarters. This suggests that the diversification push will likely be gradual rather than immediate. Though the customer mix is expected to vary quarter to quarter, hyperscaler spending will remain central to revenue growth given their scale.

Overall, Credo’s concentration risk is unlikely to disappear overnight, but the company is clearly moving toward a more balanced customer base, which could meaningfully reduce this risk over time.

Taking a Look at Rivals’ Hyperscaler Ties

Broadcom (AVGO - Free Report) sees massive opportunities in the AI space, as its hyperscaler customers have begun developing their own custom accelerators or XPUs. The company is building custom silicon platforms and enabling massive compute deployments for leading hyperscalers such as Meta, as well as AI companies like Anthropic and OpenAI.

For OpenAI, AVGO has a contractual commitment to deploy 1.3 gigawatts in 2027 as part of the wider 10-gigawatt agreement by 2029. AVGO announced an agreement with Meta in April under which it would deliver multiple generations of MTIA XPUs and deploy 3 gigawatts by 2028.

AI semiconductor revenues are expected to reach $16 billion in the third quarter of fiscal 2026, up more than 200% year over year.

Marvell Technology’s (MRVL - Free Report) hyperscaler exposure remains central to its growth strategy. On the last earnings call, management highlighted that it now ships DCI solutions to all five major U.S. hyperscalers. It expects to gain from rising demand, driven by large-scale AI clusters that increasingly span several data centers. This shift is accelerating bandwidth needs and driving adoption of higher-speed interconnect solutions like 800G and 1.6T.

Marvell noted that it is engaged with multiple Tier 1 hyperscalers across emerging areas such as scale-up networks, AECs and XPUs. While hyperscaler traction underscores strong revenue visibility, it also highlights risks stemming from reliance on hyperscaler capex cycles.

CRDO’s Price Performance, Valuation and Estimates

Shares of CRDO have gained 19.7% in the past month, while the Electronics-Semiconductors industry is up 5.4%.

p>

Image Source: Zacks Investment Research

In terms of the forward 12-month price/sales ratio, CRDO is trading at 17.71, higher than the Electronic-Semiconductors industry’s multiple of 9.14.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for CRDO’s earnings for fiscal 2027 has been revised upward over the past 60 days.

Image Source: Zacks Investment Research

CRDO currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.