We use cookies to understand how you use our site and to improve your experience. This includes personalizing content and advertising. To learn more, click here. By continuing to use our site, you accept our use of cookies, revised Privacy Policy and Terms of Service.

You are being directed to ZacksTrade, a division of LBMZ Securities and licensed broker-dealer. ZacksTrade and Zacks.com are separate companies. The web link between the two companies is not a solicitation or offer to invest in a particular security or type of security. ZacksTrade does not endorse or adopt any particular investment strategy, any analyst opinion/rating/report or any approach to evaluating individual securities.

If you wish to go to ZacksTrade, click OK. If you do not, click Cancel.

Why Should You Hold Molina Healthcare (MOH) in Your Portfolio?

Read MoreHide Full Article

Molina Healthcare, Inc. (MOH - Free Report) has been in investors’ good books owing to restructuring measures and a solid membership enrollment.

Over the past 30 days, the stock has witnessed its 2022 earnings estimates move 1.5% north.

The stock carries a VGM Score of A. Here V stands for Value, G for Growth and M for Momentum with the score being a weighted combination of all the three factors.

Its return on equity — a profitability measure — is 28.5%, better than the industry average of 19.4%. The metric reflects the presently Zacks Rank #3 (Hold) company’s effectiveness in utilizing its shareholders’ money. You can seethe complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Now let's dig deeper and see which factors make this leading health insurance company an investor favorite.

Molina Healthcare is well-poised for growth on the back of its well-diversified portfolio of state contracts across all the Medicaid product suite. It is also gaining traction from its operational efficiency.

The health insurance company continues to witness growth in its revenue base on the back of its membership growth and higher premium revenues. In the first half of the current year, its revenues climbed 45.3% year over year. Total revenues for 2021 are now anticipated to be above $26 billion compared with the prior outlook of more than $25 billion.

On the back of contract wins and strategic initiatives, its membership grew 21% and 32% year over year in 2020 and during the first half of 2021, respectively. Its series of acquisitions, such as that of YourCare led to membership growth for the company.

Molina Healthcare completed the buyout of Magellan Complete Care line of business of Magellan Health in 2020. The transaction will serve more than 3.6 million members under government-sponsored healthcare programs across 18 states. With this addition, the company is expected to build a better portfolio and gain an enhanced geographic diversity, etc.

In September 2020, Molina Healthcare inked a deal to buy substantially all the assets of Affinity Health Plan, Inc., which is expected to close in the fourth quarter of 2021. The company is also expected to complete the Cigna buyout. All these initiatives bode well for the long haul.

Concurrent with second-quarter results, the health insurer even raised its 2021 outlook. Adjusted EPS is now estimated to be $13.25 (compared with the prior guidance of at least $13 per share). Premium revenues are projected to be more than $25 billion (compared with more than $24 billion guided previously), which indicates growth of roughly 37% from the year-ago reported figure.

Total revenues for 2021 are forecast to be more than $26 billion (compared with above $25 billion expected earlier), which suggests growth of around 34% from the year-ago reported number. Membership of the company is projected to be 3.9 million, which implies a rise of 2.6% from the 2020 reported figure.

However, the health insurance provider is persistently witnessing a muted marketplace performance, which is a concern.

Its long-term growth rate stands at 17.7%, higher than the industry's average of 13.9%.

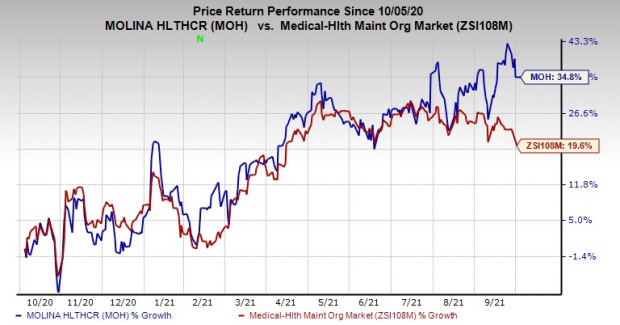

Price Performance

Shares of this company have rallied 34.8% in a year’s time, outperforming its industry’s growth of 19.6%. Image Source: Zacks Investment Research

Other companies in the same space, such as The Joint Corp. (JYNT - Free Report) , Anthem Inc. and UnitedHealth Group Incorporated (UNH - Free Report) have also gained 432.9%, 32% and 23.4%, respectively, in the same time frame.

See More Zacks Research for These Tickers

Pick one free report - opportunity may be withdrawn at any time

Image: Bigstock

Why Should You Hold Molina Healthcare (MOH) in Your Portfolio?

Molina Healthcare, Inc. (MOH - Free Report) has been in investors’ good books owing to restructuring measures and a solid membership enrollment.

Over the past 30 days, the stock has witnessed its 2022 earnings estimates move 1.5% north.

The stock carries a VGM Score of A. Here V stands for Value, G for Growth and M for Momentum with the score being a weighted combination of all the three factors.

Its return on equity — a profitability measure — is 28.5%, better than the industry average of 19.4%. The metric reflects the presently Zacks Rank #3 (Hold) company’s effectiveness in utilizing its shareholders’ money. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Now let's dig deeper and see which factors make this leading health insurance company an investor favorite.

Molina Healthcare is well-poised for growth on the back of its well-diversified portfolio of state contracts across all the Medicaid product suite. It is also gaining traction from its operational efficiency.

The health insurance company continues to witness growth in its revenue base on the back of its membership growth and higher premium revenues. In the first half of the current year, its revenues climbed 45.3% year over year. Total revenues for 2021 are now anticipated to be above $26 billion compared with the prior outlook of more than $25 billion.

On the back of contract wins and strategic initiatives, its membership grew 21% and 32% year over year in 2020 and during the first half of 2021, respectively. Its series of acquisitions, such as that of YourCare led to membership growth for the company.

Molina Healthcare completed the buyout of Magellan Complete Care line of business of Magellan Health in 2020. The transaction will serve more than 3.6 million members under government-sponsored healthcare programs across 18 states. With this addition, the company is expected to build a better portfolio and gain an enhanced geographic diversity, etc.

In September 2020, Molina Healthcare inked a deal to buy substantially all the assets of Affinity Health Plan, Inc., which is expected to close in the fourth quarter of 2021. The company is also expected to complete the Cigna buyout. All these initiatives bode well for the long haul.

Concurrent with second-quarter results, the health insurer even raised its 2021 outlook. Adjusted EPS is now estimated to be $13.25 (compared with the prior guidance of at least $13 per share). Premium revenues are projected to be more than $25 billion (compared with more than $24 billion guided previously), which indicates growth of roughly 37% from the year-ago reported figure.

Total revenues for 2021 are forecast to be more than $26 billion (compared with above $25 billion expected earlier), which suggests growth of around 34% from the year-ago reported number. Membership of the company is projected to be 3.9 million, which implies a rise of 2.6% from the 2020 reported figure.

However, the health insurance provider is persistently witnessing a muted marketplace performance, which is a concern.

Its long-term growth rate stands at 17.7%, higher than the industry's average of 13.9%.

Price Performance

Shares of this company have rallied 34.8% in a year’s time, outperforming its industry’s growth of 19.6%.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Other companies in the same space, such as The Joint Corp. (JYNT - Free Report) , Anthem Inc. and UnitedHealth Group Incorporated (UNH - Free Report) have also gained 432.9%, 32% and 23.4%, respectively, in the same time frame.