We use cookies to understand how you use our site and to improve your experience. This includes personalizing content and advertising. To learn more, click here. By continuing to use our site, you accept our use of cookies, revised Privacy Policy and Terms of Service.

You are being directed to ZacksTrade, a division of LBMZ Securities and licensed broker-dealer. ZacksTrade and Zacks.com are separate companies. The web link between the two companies is not a solicitation or offer to invest in a particular security or type of security. ZacksTrade does not endorse or adopt any particular investment strategy, any analyst opinion/rating/report or any approach to evaluating individual securities.

If you wish to go to ZacksTrade, click OK. If you do not, click Cancel.

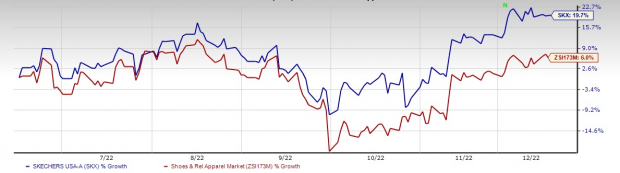

Skechers U.S.A., Inc. (SKX - Free Report) looks well-poised for growth, thanks to its focus on boosting omnichannel growth via expanding the direct-to-consumer business and enhancing its international foothold. SKX has been gaining from growth in its domestic and international channels for a while. In addition, continued global demand for its Comfort Technology footwear remains a key driver. These initiatives have aided this Zacks Rank #3 (Hold) stock to increase 19.7% in the past six months, outperforming the industry’s 6% growth.

Let’s Delve Deeper

Skechers has been directing resources to enhance its digital capabilities along with the advancement of its websites, mobile application and loyalty program. Management has updated its point-of-sale systems to better engage with customers, both offline and online. Initiatives such as “Buy Online, Pick-Up in Store” and “Buy Online, Pickup at Curbside” are worth mentioning. Investments made to integrate store and digital ecosystems for developing a seamless omnichannel experience are likely to drive greater sales. In addition, Skechers has been enhancing its distribution facilities and supply-chain production capabilities.

We note that a solid double-digit increase in the digital commerce channels aided domestic DTC sales growth in the third quarter of 2022. During the reported quarter, Skechers continued the rollout of its e-commerce platform. Management launched e-commerce sites in Poland, Switzerland and Japan. It intends to launch more e-commerce sites in the coming year.

Skechers continues to offer a diversified portfolio of brands that includes a wide range of fashion, athletic, non-athletic, and work footwear at compelling prices. We believe that this multi-brand strategy enables the company to roll out new products and reach a wide range of customers. Additionally, the company is focusing on comfort-based footwear and apparel products as consumers are embracing a relaxed lifestyle.

Image Source: Zacks Investment Research

Furthermore, Skechers’ international business remains a significant sales driver for the company. The company is poised to enhance its global reach in the footwear market through its distribution networks, subsidiaries and joint ventures. In third-quarter 2022, international sales increased 24.6% year over year. Region-wise, sales increased 16.2% year over year to $948 million in the Americas and 47.6% to $469.8 million in EMEA. The metric grew 8.6% year over year to $460.6 million in APAC.

We believe that a greater emphasis on the new line of products, cost-containment efforts, inventory management and the global distribution platform is likely to keep driving SKX’s results ahead. Skechers had envisioned fourth-quarter 2022 sales between $1.725 billion and $1.775 billion and earnings of 30-40 cents a share. In the earlier year, the company posted sales of $1.77 billion and earnings per share of 34 cents.

The Zacks Consensus Estimate for Designer Brands’ current financial-year revenues and earnings per share (EPS) suggests growth of 5.2% and 4.7%, respectively, from the corresponding year-ago reported figures. DBI has a trailing four-quarter earnings surprise of 32%, on average.

Delta Apparel is a manufacturer of active wear and lifestyle apparel products. DLA has a Zacks Rank #2 (Buy) at present.

The Zacks Consensus Estimate for Delta Apparel’s current financial-year sales suggests growth of 6.3% from the year-ago corresponding figure. DLA has a trailing four-quarter earnings surprise of 7%, on average.

Caleres, a footwear dealer, has a Zacks Rank of 2 at present. CAL has a trailing four-quarter earnings surprise of 26%, on average.

The Zacks Consensus Estimate for Caleres’ current financial-year sales and EPS suggests growth of 5.7% and 1.6%, respectively, from the year-ago corresponding figures.

Unique Zacks Analysis of Your Chosen Ticker

Pick one free report - opportunity may be withdrawn at any time

Image: Bigstock

Skechers (SKX) Omnichannel Initiatives Appear Robust

Skechers U.S.A., Inc. (SKX - Free Report) looks well-poised for growth, thanks to its focus on boosting omnichannel growth via expanding the direct-to-consumer business and enhancing its international foothold. SKX has been gaining from growth in its domestic and international channels for a while. In addition, continued global demand for its Comfort Technology footwear remains a key driver. These initiatives have aided this Zacks Rank #3 (Hold) stock to increase 19.7% in the past six months, outperforming the industry’s 6% growth.

Let’s Delve Deeper

Skechers has been directing resources to enhance its digital capabilities along with the advancement of its websites, mobile application and loyalty program. Management has updated its point-of-sale systems to better engage with customers, both offline and online. Initiatives such as “Buy Online, Pick-Up in Store” and “Buy Online, Pickup at Curbside” are worth mentioning. Investments made to integrate store and digital ecosystems for developing a seamless omnichannel experience are likely to drive greater sales. In addition, Skechers has been enhancing its distribution facilities and supply-chain production capabilities.

We note that a solid double-digit increase in the digital commerce channels aided domestic DTC sales growth in the third quarter of 2022. During the reported quarter, Skechers continued the rollout of its e-commerce platform. Management launched e-commerce sites in Poland, Switzerland and Japan. It intends to launch more e-commerce sites in the coming year.

Skechers continues to offer a diversified portfolio of brands that includes a wide range of fashion, athletic, non-athletic, and work footwear at compelling prices. We believe that this multi-brand strategy enables the company to roll out new products and reach a wide range of customers. Additionally, the company is focusing on comfort-based footwear and apparel products as consumers are embracing a relaxed lifestyle.

Image Source: Zacks Investment Research

Furthermore, Skechers’ international business remains a significant sales driver for the company. The company is poised to enhance its global reach in the footwear market through its distribution networks, subsidiaries and joint ventures. In third-quarter 2022, international sales increased 24.6% year over year. Region-wise, sales increased 16.2% year over year to $948 million in the Americas and 47.6% to $469.8 million in EMEA. The metric grew 8.6% year over year to $460.6 million in APAC.

We believe that a greater emphasis on the new line of products, cost-containment efforts, inventory management and the global distribution platform is likely to keep driving SKX’s results ahead. Skechers had envisioned fourth-quarter 2022 sales between $1.725 billion and $1.775 billion and earnings of 30-40 cents a share. In the earlier year, the company posted sales of $1.77 billion and earnings per share of 34 cents.

Stocks to Consider

Here we have highlighted three better-ranked stocks, namely, Designer Brands (DBI - Free Report) , Delta Apparel (DLA - Free Report) and Caleres (CAL - Free Report) .

Designer Brands designs, manufactures, and retails footwear and accessories. The stock currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Designer Brands’ current financial-year revenues and earnings per share (EPS) suggests growth of 5.2% and 4.7%, respectively, from the corresponding year-ago reported figures. DBI has a trailing four-quarter earnings surprise of 32%, on average.

Delta Apparel is a manufacturer of active wear and lifestyle apparel products. DLA has a Zacks Rank #2 (Buy) at present.

The Zacks Consensus Estimate for Delta Apparel’s current financial-year sales suggests growth of 6.3% from the year-ago corresponding figure. DLA has a trailing four-quarter earnings surprise of 7%, on average.

Caleres, a footwear dealer, has a Zacks Rank of 2 at present. CAL has a trailing four-quarter earnings surprise of 26%, on average.

The Zacks Consensus Estimate for Caleres’ current financial-year sales and EPS suggests growth of 5.7% and 1.6%, respectively, from the year-ago corresponding figures.