We use cookies to understand how you use our site and to improve your experience.

This includes personalizing content and advertising.

By pressing "Accept All" or closing out of this banner, you consent to the use of all cookies and similar technologies and the sharing of information they collect with third parties.

You can reject marketing cookies by pressing "Deny Optional," but we still use essential, performance, and functional cookies.

In addition, whether you "Accept All," Deny Optional," click the X or otherwise continue to use the site, you accept our Privacy Policy and Terms of Service, revised from time to time.

You are being directed to ZacksTrade, a division of LBMZ Securities and licensed broker-dealer. ZacksTrade and Zacks.com are separate companies. The web link between the two companies is not a solicitation or offer to invest in a particular security or type of security. ZacksTrade does not endorse or adopt any particular investment strategy, any analyst opinion/rating/report or any approach to evaluating individual securities.

If you wish to go to ZacksTrade, click OK. If you do not, click Cancel.

Are U.S. Tariffs a Structural Headwind for lululemon's Margins?

Read MoreHide Full Article

Key Takeaways

lululemon faces tariffs as a structural cost, pressuring margins and weighing on profitability.

LULU Q4 gross margin fell 550 bps, hurt by markdowns, tariffs and higher SG&A expenses.

lululemon expects $380M tariff costs in 2026, offset partly by $160M efficiency gains.

lululemon athletica inc. (LULU - Free Report) is facing U.S. tariffs as a structural headwind to its margins, although the impact can be partly managed through strategies and cost-control execution. Tariffs have become a significant cost pressure for the company. Such costs are expected to persist, making them a structural element within the company’s cost base. Consequently, these are adding up to extra costs, and weighing on gross margins and overall profitability.

During fourth-quarter fiscal 2025 results, although revenues and earnings per share (EPS) beat the Zacks Consensus Estimate, the bottom line fell year over year, reflecting margin pressure from higher markdowns, tariff-related costs and elevated selling, general and administrative expenses.

The gross profit dipped 8% year over year while the gross margin contracted 550 basis points (bps) in the same quarter, primarily affected by a 560-bps decline in the product margin, led by increased markdowns and tariff impacts. Tariffs had a gross negative impact of 520 bps in the quarter, partly offset by 110 bps from enterprise efficiency initiatives. Notably, markdowns increased 130 bps and fixed-cost deleverage weighed by 30 bps.

In fiscal 2025, the company incurred gross tariff expenses of $275 million. Through targeted mitigation strategies, including sourcing adjustments and cost efficiencies, the company offset $62 million of this burden, outperforming the initial expectations. Tariff pressures are expected to intensify, with gross costs projected to reach $380 million in fiscal 2026. To counter this, the company plans to leverage its enterprise-wide efficiency initiatives, which are anticipated to generate $160 million in offsets within the gross margin, helping cushion the overall impact.

The company has been working to mitigate the impact. Efforts such as improving full-price sales, reducing markdowns, optimizing inventory and diversifying its supply chain are helping to somewhat offset the tariff burden. While tariff costs cannot be fully avoided, effective execution and strategic adjustments can help partially contain their impact.

LULU’s Competition

NIKE, Inc. (NKE - Free Report) has been witnessing tariff-related costs, which have been weighing on its near-term profitability. In the third quarter of fiscal 2026, NIKE reported gross margin contraction of 130 bps, primarily reflecting a 300-bps impact from higher tariffs in North America. Regional trends further underscored the pressure, with North America’s gross margin declining 360 bps despite facing nearly 650 bps of tariff-related headwinds. NKE expects fourth-quarter gross margin to decline 25-75 bps, including roughly 250 bps of tariff impact. Management expects tariff pressures to remain a material drag through the first quarter of fiscal 2027, with margin expansion anticipated beginning in the second quarter as mitigation strategies gain traction and transitory costs subside.

adidas AG (ADDYY - Free Report) is navigating tariff risks, currency volatility and ongoing promotional intensity across the global markets. ADDYY is actively expanding its global presence by introducing locally relevant product lines and strengthening its brand equity through strategic collaborations and targeted marketing campaigns. adidas has been diversifying its supply chain and implementing risk-mitigation strategies. As supply-chain efficiencies improve and tariff exposure becomes more stable, these efforts are expected to drive adidas’ margins.

LULU’s Price Performance, Valuation and Estimates

Shares of lululemon have lost 10.1% in the past six months compared with the industry’s decline of 7.1%.

Image Source: Zacks Investment Research

From a valuation standpoint, LULU trades at a forward price-to-earnings ratio of 12.45X compared with the industry’s average of 17.16X.

Image Source: Zacks Investment Research

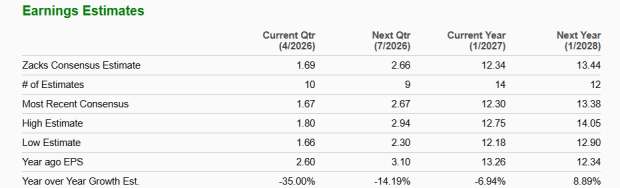

The Zacks Consensus Estimate for LULU’s fiscal 2026 earnings implies a year-over-year drop of 6.9%, while that of fiscal 2027 shows growth of 8.9%. The company’s EPS estimate for fiscal 2026 and 2027 has moved down in the past 30 days. Image Source: Zacks Investment Research

Image: Bigstock

Are U.S. Tariffs a Structural Headwind for lululemon's Margins?

Key Takeaways

lululemon athletica inc. (LULU - Free Report) is facing U.S. tariffs as a structural headwind to its margins, although the impact can be partly managed through strategies and cost-control execution. Tariffs have become a significant cost pressure for the company. Such costs are expected to persist, making them a structural element within the company’s cost base. Consequently, these are adding up to extra costs, and weighing on gross margins and overall profitability.

During fourth-quarter fiscal 2025 results, although revenues and earnings per share (EPS) beat the Zacks Consensus Estimate, the bottom line fell year over year, reflecting margin pressure from higher markdowns, tariff-related costs and elevated selling, general and administrative expenses.

The gross profit dipped 8% year over year while the gross margin contracted 550 basis points (bps) in the same quarter, primarily affected by a 560-bps decline in the product margin, led by increased markdowns and tariff impacts. Tariffs had a gross negative impact of 520 bps in the quarter, partly offset by 110 bps from enterprise efficiency initiatives. Notably, markdowns increased 130 bps and fixed-cost deleverage weighed by 30 bps.

In fiscal 2025, the company incurred gross tariff expenses of $275 million. Through targeted mitigation strategies, including sourcing adjustments and cost efficiencies, the company offset $62 million of this burden, outperforming the initial expectations. Tariff pressures are expected to intensify, with gross costs projected to reach $380 million in fiscal 2026. To counter this, the company plans to leverage its enterprise-wide efficiency initiatives, which are anticipated to generate $160 million in offsets within the gross margin, helping cushion the overall impact.

The company has been working to mitigate the impact. Efforts such as improving full-price sales, reducing markdowns, optimizing inventory and diversifying its supply chain are helping to somewhat offset the tariff burden. While tariff costs cannot be fully avoided, effective execution and strategic adjustments can help partially contain their impact.

LULU’s Competition

NIKE, Inc. (NKE - Free Report) has been witnessing tariff-related costs, which have been weighing on its near-term profitability. In the third quarter of fiscal 2026, NIKE reported gross margin contraction of 130 bps, primarily reflecting a 300-bps impact from higher tariffs in North America. Regional trends further underscored the pressure, with North America’s gross margin declining 360 bps despite facing nearly 650 bps of tariff-related headwinds. NKE expects fourth-quarter gross margin to decline 25-75 bps, including roughly 250 bps of tariff impact. Management expects tariff pressures to remain a material drag through the first quarter of fiscal 2027, with margin expansion anticipated beginning in the second quarter as mitigation strategies gain traction and transitory costs subside.

adidas AG (ADDYY - Free Report) is navigating tariff risks, currency volatility and ongoing promotional intensity across the global markets. ADDYY is actively expanding its global presence by introducing locally relevant product lines and strengthening its brand equity through strategic collaborations and targeted marketing campaigns. adidas has been diversifying its supply chain and implementing risk-mitigation strategies. As supply-chain efficiencies improve and tariff exposure becomes more stable, these efforts are expected to drive adidas’ margins.

LULU’s Price Performance, Valuation and Estimates

Shares of lululemon have lost 10.1% in the past six months compared with the industry’s decline of 7.1%.

Image Source: Zacks Investment Research

From a valuation standpoint, LULU trades at a forward price-to-earnings ratio of 12.45X compared with the industry’s average of 17.16X.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for LULU’s fiscal 2026 earnings implies a year-over-year drop of 6.9%, while that of fiscal 2027 shows growth of 8.9%. The company’s EPS estimate for fiscal 2026 and 2027 has moved down in the past 30 days.

Image Source: Zacks Investment Research

lululemon stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.