We use cookies to understand how you use our site and to improve your experience.

This includes personalizing content and advertising.

By pressing "Accept All" or closing out of this banner, you consent to the use of all cookies and similar technologies and the sharing of information they collect with third parties.

You can reject marketing cookies by pressing "Deny Optional," but we still use essential, performance, and functional cookies.

In addition, whether you "Accept All," Deny Optional," click the X or otherwise continue to use the site, you accept our Privacy Policy and Terms of Service, revised from time to time.

You are being directed to ZacksTrade, a division of LBMZ Securities and licensed broker-dealer. ZacksTrade and Zacks.com are separate companies. The web link between the two companies is not a solicitation or offer to invest in a particular security or type of security. ZacksTrade does not endorse or adopt any particular investment strategy, any analyst opinion/rating/report or any approach to evaluating individual securities.

If you wish to go to ZacksTrade, click OK. If you do not, click Cancel.

Eli Lilly became the first pharmaceutical company to top $1 trillion in market value in 2025.

An aging population and improvements in technology are fueling the growth and promise of pharma stocks.

The best pharmaceutical stocks to buy now include five companies with promising drug pipelines.

Eli Lilly (LLY), the Indianapolis-based drugmaker, recently made news by becoming the first pharmaceutical company to top $1 trillion in market value, thanks in part to its breakout weight-loss drugs, Mounjaro and Zepbound. Are other pharma stocks worth a look?

Are Pharmaceutical Stocks a Good Investment?

Pharmaceutical firms have long been viewed as a blend of defensive income plays and growth opportunities. As demand for medicines, vaccines, and chronic-disease treatments remains steady regardless of economic cycles, pharma companies often deliver stable earnings. That stability — combined with generous dividends many pharma companies pay — makes them especially attractive when the broader market is choppy or inflation is high.

Additionally, the global pharmaceutical industry continues to grow: Analysts expect the sector to expand over the coming years, aided by rising demand for treatments for chronic illnesses, oncology, vaccines and demographic factors such as aging populations.

However, pharmaceutical investing isn’t risk-free. Outcomes often depend on R&D success, regulatory approvals, patent expirations, and competitive pressures. That’s why smart investors often balance stable dividend-payers with growth-oriented firms or diversify across multiple names.

Here, we analyze and rank the best pharmaceutical stocks to buy now ranked on a blend Zacks Rank signals, Style Scores and fundamentals:

This is our short term rating system that serves as a timeliness indicator for stocks over the next 1 to 3 months. How good is it? See rankings and related performance below.

The Zacks Industry Rank assigns a rating to each of the 265 X (Expanded) Industries based on their average Zacks Rank.

An industry with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The industry with the best average Zacks Rank would be considered the top industry (1 out of 265), which would place it in the top 1% of Zacks Ranked Industries. The industry with the worst average Zacks Rank (265 out of 265) would place in the bottom 1%.

The Zacks Sector Rank assigns a rating to each of the 16 Sectors based on their average Zacks Rank.

A sector with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The sector with the best average Zacks Rank would be considered the top sector (1 out of 16), which would place it in the top 1% of Zacks Ranked Sectors. The sector with the worst average Zacks Rank (16 out of 16) would place in the bottom 1%.

The Style Scores are a complementary set of indicators to use alongside the Zacks Rank. It allows the user to better focus on the stocks that are the best fit for his or her personal trading style.

The scores are based on the trading styles of Value, Growth, and Momentum. There's also a VGM Score ('V' for Value, 'G' for Growth and 'M' for Momentum), which combines the weighted average of the individual style scores into one score.

Value ScoreA

Growth ScoreA

Momentum ScoreA

VGM ScoreA

Within each Score, stocks are graded into five groups: A, B, C, D and F. As you might remember from your school days, an A, is better than a B; a B is better than a C; a C is better than a D; and a D is better than an F.

As an investor, you want to buy stocks with the highest probability of success. That means you want to buy stocks with a Zacks Rank #1 or #2, Strong Buy or Buy, which also has a Score of an A or a B in your personal trading style.

Zacks Earnings ESP (Expected Surprise Prediction) looks to find companies that have recently seen positive earnings estimate revision activity. The idea is that more recent information is, generally speaking, more accurate and can be a better predictor of the future, which can give investors an advantage in earnings season.

The technique has proven to be very useful for finding positive surprises. In fact, when combining a Zacks Rank #3 or better and a positive Earnings ESP, stocks produced a positive surprise 70% of the time, while they also saw 28.3% annual returns on average, according to our 10 year backtest.

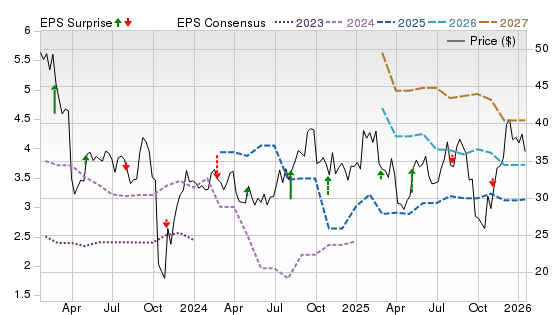

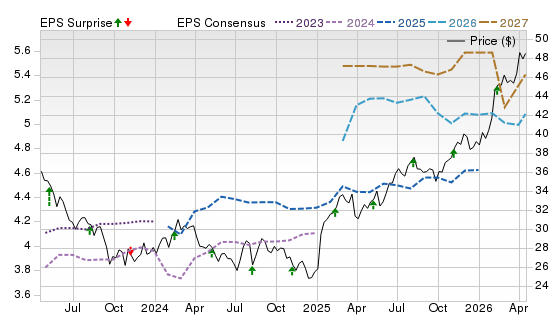

Harmony Biosciences develops therapies for rare neurological disorders, with WAKIX driving its current pharmaceutical revenue. The company’s preliminary Q2 2026 results reflect that WAKIX sales rose 30% year over year to about $261 million, extending first-quarter growth and supporting management’s $1.0-$1.04 billion full-year target. Pitolisant lifecycle programs and the BP-205 orexin-2 agonist could potentially broaden the franchise beyond narcolepsy meaningfully over time.

Potential Risks

WAKIX concentration leaves earnings exposed to payer access, narcolepsy demand, and patent litigation. Generic challenges, clinical setbacks, commercialization spending, or management turnover could quickly pressure expectations.

Forecast

A Zacks Rank #1 (Strong Buy) with Scores of A for Value and VGM signals attractive revisions and valuation. The company's Price, Consensus & EPS Surprise chart shows a volatile price action, declining 2026-2027 EPS consensus lines, and a mixed earnings surprise pattern.

This is our short term rating system that serves as a timeliness indicator for stocks over the next 1 to 3 months. How good is it? See rankings and related performance below.

The Zacks Industry Rank assigns a rating to each of the 265 X (Expanded) Industries based on their average Zacks Rank.

An industry with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The industry with the best average Zacks Rank would be considered the top industry (1 out of 265), which would place it in the top 1% of Zacks Ranked Industries. The industry with the worst average Zacks Rank (265 out of 265) would place in the bottom 1%.

The Zacks Sector Rank assigns a rating to each of the 16 Sectors based on their average Zacks Rank.

A sector with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The sector with the best average Zacks Rank would be considered the top sector (1 out of 16), which would place it in the top 1% of Zacks Ranked Sectors. The sector with the worst average Zacks Rank (16 out of 16) would place in the bottom 1%.

The Style Scores are a complementary set of indicators to use alongside the Zacks Rank. It allows the user to better focus on the stocks that are the best fit for his or her personal trading style.

The scores are based on the trading styles of Value, Growth, and Momentum. There's also a VGM Score ('V' for Value, 'G' for Growth and 'M' for Momentum), which combines the weighted average of the individual style scores into one score.

Value ScoreA

Growth ScoreA

Momentum ScoreA

VGM ScoreA

Within each Score, stocks are graded into five groups: A, B, C, D and F. As you might remember from your school days, an A, is better than a B; a B is better than a C; a C is better than a D; and a D is better than an F.

As an investor, you want to buy stocks with the highest probability of success. That means you want to buy stocks with a Zacks Rank #1 or #2, Strong Buy or Buy, which also has a Score of an A or a B in your personal trading style.

Zacks Earnings ESP (Expected Surprise Prediction) looks to find companies that have recently seen positive earnings estimate revision activity. The idea is that more recent information is, generally speaking, more accurate and can be a better predictor of the future, which can give investors an advantage in earnings season.

The technique has proven to be very useful for finding positive surprises. In fact, when combining a Zacks Rank #3 or better and a positive Earnings ESP, stocks produced a positive surprise 70% of the time, while they also saw 28.3% annual returns on average, according to our 10 year backtest.

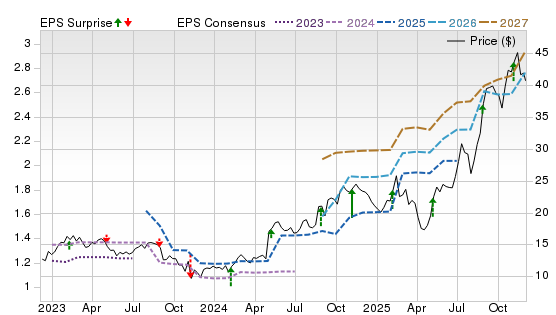

Phibro Animal Health sells vaccines, medicated feed additives and nutritional products for livestock and companion animals. Its broad portfolio benefits from recurring demand tied to animal health, food production and disease prevention. The company’s Zoetis medicated feed additive assets broaden its product lineup, geographic reach and customer relationships, while strength in the animal health business and continued vaccine adoption offer additional earnings and cash flow potential.

Potential Risks

Brazilian antimicrobial regulation, elevated leverage, freight and currency costs could erode gains. Weak demand across its performance products business and rising employee or interest expense add pressure.

Forecast

A Zacks Rank #2 (Buy) with a Score of A for Value points to favorable near-term revisions and valuation support, despite Scores of F for Growth and Momentum. The chart shows a strong price uptrend with a recent pullback, while consensus estimates sharply rise into 2026-2028, and recent surprises skew positive.

This is our short term rating system that serves as a timeliness indicator for stocks over the next 1 to 3 months. How good is it? See rankings and related performance below.

The Zacks Industry Rank assigns a rating to each of the 265 X (Expanded) Industries based on their average Zacks Rank.

An industry with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The industry with the best average Zacks Rank would be considered the top industry (1 out of 265), which would place it in the top 1% of Zacks Ranked Industries. The industry with the worst average Zacks Rank (265 out of 265) would place in the bottom 1%.

The Zacks Sector Rank assigns a rating to each of the 16 Sectors based on their average Zacks Rank.

A sector with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The sector with the best average Zacks Rank would be considered the top sector (1 out of 16), which would place it in the top 1% of Zacks Ranked Sectors. The sector with the worst average Zacks Rank (16 out of 16) would place in the bottom 1%.

The Style Scores are a complementary set of indicators to use alongside the Zacks Rank. It allows the user to better focus on the stocks that are the best fit for his or her personal trading style.

The scores are based on the trading styles of Value, Growth, and Momentum. There's also a VGM Score ('V' for Value, 'G' for Growth and 'M' for Momentum), which combines the weighted average of the individual style scores into one score.

Value ScoreA

Growth ScoreA

Momentum ScoreA

VGM ScoreA

Within each Score, stocks are graded into five groups: A, B, C, D and F. As you might remember from your school days, an A, is better than a B; a B is better than a C; a C is better than a D; and a D is better than an F.

As an investor, you want to buy stocks with the highest probability of success. That means you want to buy stocks with a Zacks Rank #1 or #2, Strong Buy or Buy, which also has a Score of an A or a B in your personal trading style.

Zacks Earnings ESP (Expected Surprise Prediction) looks to find companies that have recently seen positive earnings estimate revision activity. The idea is that more recent information is, generally speaking, more accurate and can be a better predictor of the future, which can give investors an advantage in earnings season.

The technique has proven to be very useful for finding positive surprises. In fact, when combining a Zacks Rank #3 or better and a positive Earnings ESP, stocks produced a positive surprise 70% of the time, while they also saw 28.3% annual returns on average, according to our 10 year backtest.

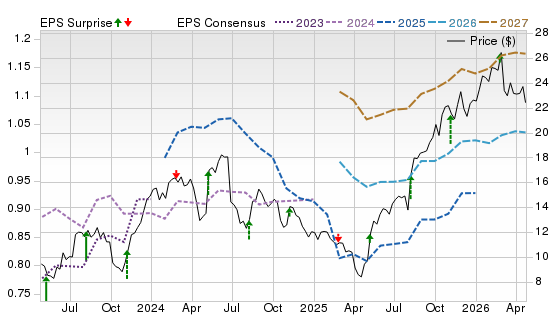

Elanco Animal Health develops medicines, vaccines and parasiticides for pets and livestock, providing broad exposure to the global animal-health market. The company benefits from growing adoption of its new offerings like Zenrelia and Credelio Quattro, while portfolio simplification, productivity initiatives and debt reduction offer scope for stronger margins and cash flow. Long-term demand is also supported by rising pet care spending and the requirement to improve livestock health and efficiency.

Potential Risks

Livestock demand is exposed to farm economics and disease cycles, and competitive pet-health launches can erode share. Elevated debt, foreign exchange, and regulatory scrutiny could also limit upside.

Forecast

A Zacks Rank #3 (Hold) with Scores of B for Growth, and C for Value and Momentum points to improving fundamentals without a decisive valuation or price signal. The chart shows the stock rebounding strongly from prior lows as 2026-2028 consensus estimates trend upward and surprises skew positive.

This is our short term rating system that serves as a timeliness indicator for stocks over the next 1 to 3 months. How good is it? See rankings and related performance below.

The Zacks Industry Rank assigns a rating to each of the 265 X (Expanded) Industries based on their average Zacks Rank.

An industry with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The industry with the best average Zacks Rank would be considered the top industry (1 out of 265), which would place it in the top 1% of Zacks Ranked Industries. The industry with the worst average Zacks Rank (265 out of 265) would place in the bottom 1%.

The Zacks Sector Rank assigns a rating to each of the 16 Sectors based on their average Zacks Rank.

A sector with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The sector with the best average Zacks Rank would be considered the top sector (1 out of 16), which would place it in the top 1% of Zacks Ranked Sectors. The sector with the worst average Zacks Rank (16 out of 16) would place in the bottom 1%.

The Style Scores are a complementary set of indicators to use alongside the Zacks Rank. It allows the user to better focus on the stocks that are the best fit for his or her personal trading style.

The scores are based on the trading styles of Value, Growth, and Momentum. There's also a VGM Score ('V' for Value, 'G' for Growth and 'M' for Momentum), which combines the weighted average of the individual style scores into one score.

Value ScoreA

Growth ScoreA

Momentum ScoreA

VGM ScoreA

Within each Score, stocks are graded into five groups: A, B, C, D and F. As you might remember from your school days, an A, is better than a B; a B is better than a C; a C is better than a D; and a D is better than an F.

As an investor, you want to buy stocks with the highest probability of success. That means you want to buy stocks with a Zacks Rank #1 or #2, Strong Buy or Buy, which also has a Score of an A or a B in your personal trading style.

Zacks Earnings ESP (Expected Surprise Prediction) looks to find companies that have recently seen positive earnings estimate revision activity. The idea is that more recent information is, generally speaking, more accurate and can be a better predictor of the future, which can give investors an advantage in earnings season.

The technique has proven to be very useful for finding positive surprises. In fact, when combining a Zacks Rank #3 or better and a positive Earnings ESP, stocks produced a positive surprise 70% of the time, while they also saw 28.3% annual returns on average, according to our 10 year backtest.

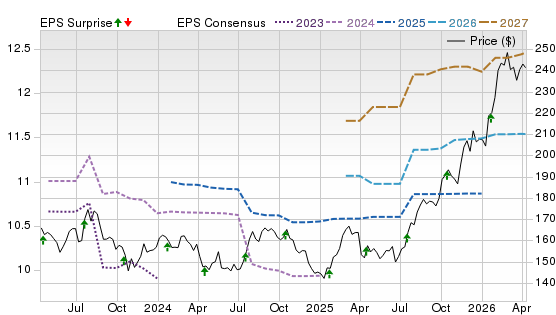

Johnson & Johnson combines innovative medicines with medical technology, providing diversified pharmaceutical exposure. In Q2 2026, the company’s Innovative Medicine operational sales grew 6.8% year over year, led by DARZALEX, CARVYKTI, TREMFYA, SPRAVATO and CAPLYTA. Management raised its 2026 outlook, underscoring portfolio breadth and sustained pipeline momentum. It has rapidly advanced its pipeline in the past year, which will help drive growth through the back half of the decade.

Potential Risks

Key risks include faster-than-expected patent erosion, drug-pricing pressure, pipeline or launch disappointments, and ongoing talc-related litigation. Recent share-price strength also raises sensitivity to any guidance miss.

Forecast

A Zacks Rank #3 indicates a neutral revision signal. While a Score of A for Momentum reflects strong price action, Scores of C for Value and Growth offer limited factor support. The chart shows a powerful price breakout alongside steadily rising 2026-2028 consensus estimates and a predominantly positive surprise history.

This is our short term rating system that serves as a timeliness indicator for stocks over the next 1 to 3 months. How good is it? See rankings and related performance below.

The Zacks Industry Rank assigns a rating to each of the 265 X (Expanded) Industries based on their average Zacks Rank.

An industry with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The industry with the best average Zacks Rank would be considered the top industry (1 out of 265), which would place it in the top 1% of Zacks Ranked Industries. The industry with the worst average Zacks Rank (265 out of 265) would place in the bottom 1%.

The Zacks Sector Rank assigns a rating to each of the 16 Sectors based on their average Zacks Rank.

A sector with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The sector with the best average Zacks Rank would be considered the top sector (1 out of 16), which would place it in the top 1% of Zacks Ranked Sectors. The sector with the worst average Zacks Rank (16 out of 16) would place in the bottom 1%.

The Style Scores are a complementary set of indicators to use alongside the Zacks Rank. It allows the user to better focus on the stocks that are the best fit for his or her personal trading style.

The scores are based on the trading styles of Value, Growth, and Momentum. There's also a VGM Score ('V' for Value, 'G' for Growth and 'M' for Momentum), which combines the weighted average of the individual style scores into one score.

Value ScoreA

Growth ScoreA

Momentum ScoreA

VGM ScoreA

Within each Score, stocks are graded into five groups: A, B, C, D and F. As you might remember from your school days, an A, is better than a B; a B is better than a C; a C is better than a D; and a D is better than an F.

As an investor, you want to buy stocks with the highest probability of success. That means you want to buy stocks with a Zacks Rank #1 or #2, Strong Buy or Buy, which also has a Score of an A or a B in your personal trading style.

Zacks Earnings ESP (Expected Surprise Prediction) looks to find companies that have recently seen positive earnings estimate revision activity. The idea is that more recent information is, generally speaking, more accurate and can be a better predictor of the future, which can give investors an advantage in earnings season.

The technique has proven to be very useful for finding positive surprises. In fact, when combining a Zacks Rank #3 or better and a positive Earnings ESP, stocks produced a positive surprise 70% of the time, while they also saw 28.3% annual returns on average, according to our 10 year backtest.

Royalty Pharma finances biopharmaceutical innovation in exchange for royalties, offering diversified exposure to approved and development-stage medicines without running commercial operations. Its portfolio spans multiple therapies, partners, and disease areas, helping reduce dependence on any single asset. Contracted royalty streams support recurring cash generation, while acquisitions and research and development funding agreements provide additional growth opportunities.

Potential Risks

Risks include concentration in large products, patent expirations, clinical or regulatory failures on development-stage assets, and overpaying for new royalties. Higher financing costs or slower deal deployment could also dilute returns.

Forecast

A Zacks Rank #3 is neutral. While Scores of B for Momentum and VGM indicate a strong relative price performance, Scores of C for Value and Growth offer limited factor support. The company’s chart shows a strong price uptrend, with rising 2026 consensus estimates and mostly favorable earnings surprises.

The Zacks Rank is a proprietary stock-rating model that uses trends in earnings estimate revisions and earnings-per-share (EPS) surprises to classify stocks into five groups: #1 (Strong Buy), #2 (Buy), #3 (Hold), #4 (Sell) and #5 (Strong Sell). The Zacks Rank is calculated through four primary factors related to earnings estimates: analysts' consensus on earnings estimate revisions, the magnitude of revision change, the upside potential and estimate surprise (or the degree in which earnings per share deviated from the previous quarter).

Zacks builds the data from 3,000 analysts at over 150 different brokerage firms. The average yearly gain for Zacks Rank #1 (Strong Buy) stocks is +23.94% per year from January, 1988, through July 6, 2026.

Selections for Best Pharmaceutical Stocks are based on the current top ranking stocks based on Zacks Indicator Score and other factors. For this list, only companies that have average daily trading volumes of 100,000 shares or more are considered. All information is current as of market open, July 31, 2026.

Learn More about Pharmaceutical Stocks

What are Pharmaceutical Stocks?

“Pharmaceutical stocks” refer to publicly traded companies engaged primarily in the discovery, development, manufacturing, and sale of drugs — including brand-name medicines, biologics, vaccines and sometimes generics.

Types of Pharmaceutical Stocks

Large-cap, established pharmaceutical companies – These are the global leaders with diverse drug portfolios, steady revenue streams, and long histories of paying dividends. Examples include Pfizer (PFE - Free Report), Merck (MRK - Free Report), Johnson & Johnson (JNJ - Free Report), AbbVie (ABBV - Free Report), Bristol-Myers Squibb (BMY - Free Report) and Novartis (NVS). These companies tend to have well-funded pipelines and wide geographic reach, making them popular with conservative investors.

Specialty-drug and focused biopharma firms – These companies concentrate on specific therapeutic areas such as rare diseases, oncology, immunology, or metabolic conditions. They can deliver strong growth if a breakthrough therapy succeeds. Examples include Vertex Pharmaceuticals (VRTX - Free Report) in genetic diseases, Regeneron (REGN - Free Report) in immunology and ophthalmology, Incyte (INCY - Free Report) in oncology and Horizon Therapeutics (HZNP - Free Report) in autoimmune disorders.

Pipeline-driven or R&D-intensive pharmaceutical developers – These companies may have fewer commercialized drugs but invest heavily in research, clinical trials, and next-generation treatments. Revenue may be uneven, but the upside can be significant if major approvals come through. Notable examples include Moderna (MRNA - Free Report) in mRNA therapeutics, BioNTech (BNTX - Free Report) in immuno-oncology, Alnylam Pharmaceuticals (ALNY - Free Report) in RNA interference drugs and Sarepta Therapeutics (SRPT - Free Report) in genetic therapies.

Pros of Pharmaceutical Stocks

Consistent demand for medicines: Healthcare needs remain steady regardless of economic cycles, helping companies like Merck, Eli Lilly (LLY - Free Report), or AstraZeneca (AZN - Free Report) maintain dependable revenue.

Attractive dividends: Many large pharmaceutical companies, such as Pfizer, AbbVie, and Johnson & Johnson, are known for long-standing dividend programs and high payout reliability.

Potential for major upside from drug launches: A successful approval or breakthrough therapy—such as Eli Lilly’s diabetes/obesity drugs or Regeneron’s eye-disease treatments—can significantly boost a company’s valuation.

Diversification within healthcare: Pharma stocks often behave differently from technology, consumer, or financial sectors, providing balance to an investment portfolio.

Cons of Pharmaceutical Stocks

Regulatory hurdles: Failure to secure FDA approval, clinical-trial setbacks, or safety concerns can sharply impact valuations when trials don’t meet expectations.

Patent cliffs and generic competition: Once exclusivity ends, branded drugs can face rapid erosion from generics or biosimilars. For instance, AbbVie’s Humira — once the world’s top-selling drug — saw sales drop after biosimilar competition entered the market.

Competitive pressures: New drugs from rivals can displace existing blockbusters. For example, Novo Nordisk (NVO - Free Report) and Eli Lilly (LLY) dominate the obesity/diabetes segment, squeezing competitors.

High research costs and uncertainties: Pharma R&D is expensive and unpredictable. Firms like Moderna, Alnylam, or Sarepta often experience stock volatility tied directly to clinical-trial outcomes or scientific feasibility.

Best Pharmaceutical Stocks vs. Biotechnology Stocks: Which Is Better?

Pharmaceutical companies (large-cap pharma) These firms—such as Merck, Pfizer, AbbVie, and Novartis—tend to be more stable due to established product lines and recurring revenue. They typically appeal to income-focused investors because they often pay strong and consistent dividends.

Biotechnology companies Biotech firms like Regeneron, Vertex, Moderna, and BioNTech often target cutting-edge scientific approaches with high growth potential. Their revenues can surge when a breakthrough therapy succeeds, but they face much greater volatility and dependency on research outcomes.

If you prefer steady dividends and lower volatility, large U.S. and international pharma names are generally a better fit.

If you’re seeking high potential returns and can handle larger price swings, biotech and R&D-intensive drug developers may offer superior upside.

Many investors blend both categories to balance income with innovation-driven growth.

Risks and Safety

How do FDA approvals impact stock prices?

Securing FDA approval for a new drug can be a major catalyst: positive news can dramatically boost stock price. Conversely, delays, negative trial results, or regulatory setbacks can result in sharp declines. That’s why even solid firms factor in “uncertainty rating” — because much hinges on regulatory success.

How do patent expirations affect pharmaceutical stocks?

When a drug’s patent expires, generics may enter, often severely reducing sales for the original drug — which can lead to revenue decline unless the company successfully replaces the lost revenue with new drugs or therapies.

What are the biggest risks when investing in drug companies?

R&D failure and sunk costs.

Regulatory hurdles and unpredictable approval processes.

Litigation, pricing pressure, changes in healthcare policy and regulation.

Concentration risk if a company relies heavily on a few blockbuster drugs.

Pharmaceutical Stocks Trends

Which pharmaceutical stock benefits the most from aging population trends?

Large-cap companies with broad portfolios — especially those offering treatments for chronic diseases (e.g., cardiovascular, cancer, auto-immune, diabetes) — tend to benefit from demographic trends. Firms like Merck, AbbVie, and others with diversified pipelines may be especially well positioned.

How have pharmaceutical stocks performed in the last 5 years?

Many large-cap pharma stocks have offered attractive dividend yields and moderate growth, often outperforming more cyclical sectors, especially in volatile markets. Their relative resilience and dividends have appealed to investors seeking stability.

Are pharma stocks recession-proof?

Not entirely — but compared with consumer discretionary or cyclical sectors, pharma tends to be more resilient. Demand for essential medicines tends to remain stable even during economic downturns, giving pharma a defensive characteristic.

How to Invest in Pharmaceutical Stocks

Should beginners invest in pharma ETFs instead of single stocks?

Yes — for many retail investors, pharma-focused ETFs (or broader healthcare ETFs) offer diversified exposure, reducing the risk of overconcentration in a single company. This mitigates risks like regulatory failure or drug-specific setbacks.

Is it better to invest in global or U.S. pharmaceutical companies?

Both have advantages. U.S. firms often lead in innovation, R&D, and large-scale global distribution. International companies may offer exposure to different markets, drug pipelines, and potentially attractive valuations. A mix of both can provide balanced diversification.

Strong Buy

Strong Buy

Hold

Hold

: The Neocloud Leader")

Stocks to Buy Now August 2026")