We use cookies to understand how you use our site and to improve your experience.

This includes personalizing content and advertising.

By pressing "Accept All" or closing out of this banner, you consent to the use of all cookies and similar technologies and the sharing of information they collect with third parties.

You can reject marketing cookies by pressing "Deny Optional," but we still use essential, performance, and functional cookies.

In addition, whether you "Accept All," Deny Optional," click the X or otherwise continue to use the site, you accept our Privacy Policy and Terms of Service, revised from time to time.

You are being directed to ZacksTrade, a division of LBMZ Securities and licensed broker-dealer. ZacksTrade and Zacks.com are separate companies. The web link between the two companies is not a solicitation or offer to invest in a particular security or type of security. ZacksTrade does not endorse or adopt any particular investment strategy, any analyst opinion/rating/report or any approach to evaluating individual securities.

If you wish to go to ZacksTrade, click OK. If you do not, click Cancel.

Stocks priced under $10 can present appealing entry points for investors seeking outsized returns.

A depressed price can mask solid businesses facing temporary headwinds, such as cyclical downturns.

Investors must separate quality cheap stocks from value traps, where structural issues cap long-term upside.

Cheap stocks trading under $10 often attract investors looking to stretch their capital, uncover turnaround stories, or gain exposure to growing industries at a lower entry point. While a low share price alone doesn’t guarantee value, many sub-$10 stocks are established businesses temporarily out of favor, emerging growth companies, or overlooked operators with improving fundamentals.

Are Cheap Stocks a Good Investment?

Stocks priced under $10 can present appealing entry points for investors seeking asymmetric returns — the potential for outsized gains relative to the initial investment. Reputable analysts and financial outlets frequently flag these names because a depressed price can mask solid businesses facing temporary earnings pressure, cyclical slowdowns, or sentiment-driven selloffs.

That said, cheap does not always mean valuable. A low price may reflect:

Temporary earnings weakness or cyclical downturns.

Industry-wide headwinds.

Cash flow constraints.

Poor management execution.

Investors must separate quality cheap stocks from value traps, where structural issues cap long-term upside. As Warren Buffett has often emphasized, a stock is only a bargain if the underlying business can earn durable profits.

Below, we analyze and rank the best cheap stocks under $10 using a blend of Zacks Rank signals, Style Scores, and fundamentals.

This is our short term rating system that serves as a timeliness indicator for stocks over the next 1 to 3 months. How good is it? See rankings and related performance below.

The Zacks Industry Rank assigns a rating to each of the 265 X (Expanded) Industries based on their average Zacks Rank.

An industry with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The industry with the best average Zacks Rank would be considered the top industry (1 out of 265), which would place it in the top 1% of Zacks Ranked Industries. The industry with the worst average Zacks Rank (265 out of 265) would place in the bottom 1%.

The Zacks Sector Rank assigns a rating to each of the 16 Sectors based on their average Zacks Rank.

A sector with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The sector with the best average Zacks Rank would be considered the top sector (1 out of 16), which would place it in the top 1% of Zacks Ranked Sectors. The sector with the worst average Zacks Rank (16 out of 16) would place in the bottom 1%.

The Style Scores are a complementary set of indicators to use alongside the Zacks Rank. It allows the user to better focus on the stocks that are the best fit for his or her personal trading style.

The scores are based on the trading styles of Value, Growth, and Momentum. There's also a VGM Score ('V' for Value, 'G' for Growth and 'M' for Momentum), which combines the weighted average of the individual style scores into one score.

Value ScoreA

Growth ScoreA

Momentum ScoreA

VGM ScoreA

Within each Score, stocks are graded into five groups: A, B, C, D and F. As you might remember from your school days, an A, is better than a B; a B is better than a C; a C is better than a D; and a D is better than an F.

As an investor, you want to buy stocks with the highest probability of success. That means you want to buy stocks with a Zacks Rank #1 or #2, Strong Buy or Buy, which also has a Score of an A or a B in your personal trading style.

Zacks Earnings ESP (Expected Surprise Prediction) looks to find companies that have recently seen positive earnings estimate revision activity. The idea is that more recent information is, generally speaking, more accurate and can be a better predictor of the future, which can give investors an advantage in earnings season.

The technique has proven to be very useful for finding positive surprises. In fact, when combining a Zacks Rank #3 or better and a positive Earnings ESP, stocks produced a positive surprise 70% of the time, while they also saw 28.3% annual returns on average, according to our 10 year backtest.

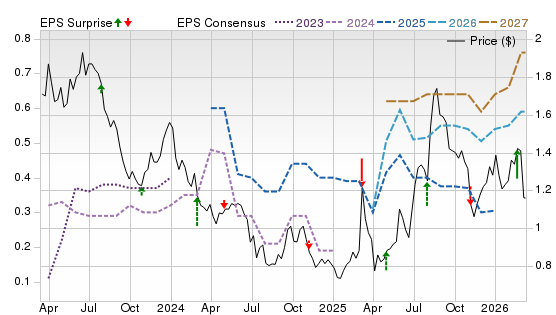

Redwood Trust is a small-cap mortgage REIT and mortgage-banking operator with a $762.4 million market cap. In Q4 2025, its mortgage banking platform posted a record $7.3 billion of production and record segment net income, while book value held at $7.36 per share. Management is shifting capital out of legacy assets and into scalable origination channels, and buybacks have been modestly accretive to book.

Potential Risks

Results are sensitive to interest-rate swings, securitization spreads and mortgage-credit performance. A housing slowdown or missteps in the legacy wind-down could pressure book value.

Forecast

A Zacks Rank #1 (Strong Buy) typically reflects upward estimate revisions. Style Scores of F for Value and Growth temper the “cheap” signal, but a C for Momentum points to stabilization. The Price, Consensus & EPS Surprise chart shows 2026–2027 EPS consensus trending higher after mixed surprises, suggesting further revisions if production holds.

This is our short term rating system that serves as a timeliness indicator for stocks over the next 1 to 3 months. How good is it? See rankings and related performance below.

The Zacks Industry Rank assigns a rating to each of the 265 X (Expanded) Industries based on their average Zacks Rank.

An industry with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The industry with the best average Zacks Rank would be considered the top industry (1 out of 265), which would place it in the top 1% of Zacks Ranked Industries. The industry with the worst average Zacks Rank (265 out of 265) would place in the bottom 1%.

The Zacks Sector Rank assigns a rating to each of the 16 Sectors based on their average Zacks Rank.

A sector with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The sector with the best average Zacks Rank would be considered the top sector (1 out of 16), which would place it in the top 1% of Zacks Ranked Sectors. The sector with the worst average Zacks Rank (16 out of 16) would place in the bottom 1%.

The Style Scores are a complementary set of indicators to use alongside the Zacks Rank. It allows the user to better focus on the stocks that are the best fit for his or her personal trading style.

The scores are based on the trading styles of Value, Growth, and Momentum. There's also a VGM Score ('V' for Value, 'G' for Growth and 'M' for Momentum), which combines the weighted average of the individual style scores into one score.

Value ScoreA

Growth ScoreA

Momentum ScoreA

VGM ScoreA

Within each Score, stocks are graded into five groups: A, B, C, D and F. As you might remember from your school days, an A, is better than a B; a B is better than a C; a C is better than a D; and a D is better than an F.

As an investor, you want to buy stocks with the highest probability of success. That means you want to buy stocks with a Zacks Rank #1 or #2, Strong Buy or Buy, which also has a Score of an A or a B in your personal trading style.

Zacks Earnings ESP (Expected Surprise Prediction) looks to find companies that have recently seen positive earnings estimate revision activity. The idea is that more recent information is, generally speaking, more accurate and can be a better predictor of the future, which can give investors an advantage in earnings season.

The technique has proven to be very useful for finding positive surprises. In fact, when combining a Zacks Rank #3 or better and a positive Earnings ESP, stocks produced a positive surprise 70% of the time, while they also saw 28.3% annual returns on average, according to our 10 year backtest.

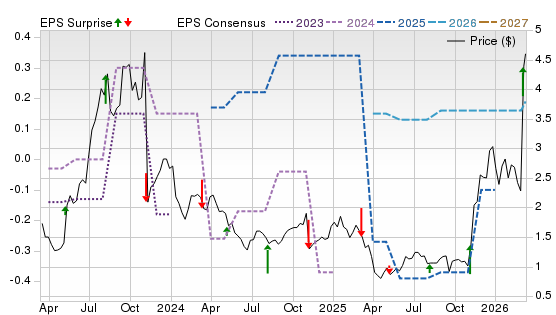

Chatham Lodging Trust is a small-cap hotel REIT focused on extended-stay and premium-branded properties, with a $373.3 million market cap. In Q4 2025, adjusted FFO rose 5% per share even as RevPAR slipped, reflecting cost control and a steady business-travel base. Management leaned into capital returns, repurchasing about 1 million shares and recycling an older asset, a mix that can matter when the stock screens cheap on cash flow and asset value.

Potential Risks

Lodging cash flows are cyclical: a slowdown in corporate travel or new supply could hit occupancy and pricing. Higher refinancing costs can weigh on levered REITs and disruptions can compress margins.

Forecast

A Zacks Rank #1, with A for Value and Momentum, suggests revisions and price action are aligned despite F for Growth. The chart shows consensus drifting lower before stabilizing into 2026 with a late upward jump after uneven surprises.

This is our short term rating system that serves as a timeliness indicator for stocks over the next 1 to 3 months. How good is it? See rankings and related performance below.

The Zacks Industry Rank assigns a rating to each of the 265 X (Expanded) Industries based on their average Zacks Rank.

An industry with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The industry with the best average Zacks Rank would be considered the top industry (1 out of 265), which would place it in the top 1% of Zacks Ranked Industries. The industry with the worst average Zacks Rank (265 out of 265) would place in the bottom 1%.

The Zacks Sector Rank assigns a rating to each of the 16 Sectors based on their average Zacks Rank.

A sector with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The sector with the best average Zacks Rank would be considered the top sector (1 out of 16), which would place it in the top 1% of Zacks Ranked Sectors. The sector with the worst average Zacks Rank (16 out of 16) would place in the bottom 1%.

The Style Scores are a complementary set of indicators to use alongside the Zacks Rank. It allows the user to better focus on the stocks that are the best fit for his or her personal trading style.

The scores are based on the trading styles of Value, Growth, and Momentum. There's also a VGM Score ('V' for Value, 'G' for Growth and 'M' for Momentum), which combines the weighted average of the individual style scores into one score.

Value ScoreA

Growth ScoreA

Momentum ScoreA

VGM ScoreA

Within each Score, stocks are graded into five groups: A, B, C, D and F. As you might remember from your school days, an A, is better than a B; a B is better than a C; a C is better than a D; and a D is better than an F.

As an investor, you want to buy stocks with the highest probability of success. That means you want to buy stocks with a Zacks Rank #1 or #2, Strong Buy or Buy, which also has a Score of an A or a B in your personal trading style.

Zacks Earnings ESP (Expected Surprise Prediction) looks to find companies that have recently seen positive earnings estimate revision activity. The idea is that more recent information is, generally speaking, more accurate and can be a better predictor of the future, which can give investors an advantage in earnings season.

The technique has proven to be very useful for finding positive surprises. In fact, when combining a Zacks Rank #3 or better and a positive Earnings ESP, stocks produced a positive surprise 70% of the time, while they also saw 28.3% annual returns on average, according to our 10 year backtest.

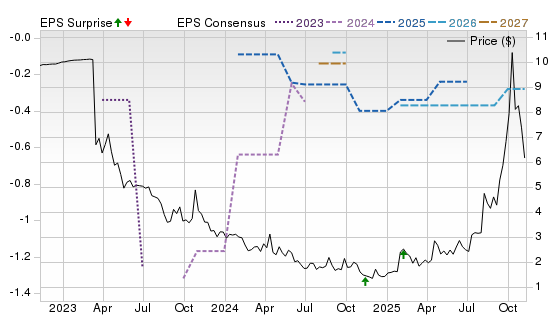

NioCorp Developments is a critical minerals developer with a $703.7 million market cap, advancing the Elk Creek niobium-scandium-titanium project in Nebraska. The company's latest preliminary data showed a record cash balance of $307 million and working capital, giving it time to fund engineering and pre-construction work. Management also cited progress in EXIM’s diligence process and steps toward a domestic scandium supply chain, including the FEA Materials' asset and IP acquisition.

Potential Risks

NB is pre-revenue and will require more capital to build Elk Creek, so dilution and schedule slippage are central risks. Critical minerals pricing, permitting and offtake execution can swing sentiment.

Forecast

A Zacks Rank #1 signals improving estimates, but F for Value and Momentum and D for Growth are a caution. The chart shows loss estimates improving into 2027 after a previous reset, with mixed surprises.

This is our short term rating system that serves as a timeliness indicator for stocks over the next 1 to 3 months. How good is it? See rankings and related performance below.

The Zacks Industry Rank assigns a rating to each of the 265 X (Expanded) Industries based on their average Zacks Rank.

An industry with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The industry with the best average Zacks Rank would be considered the top industry (1 out of 265), which would place it in the top 1% of Zacks Ranked Industries. The industry with the worst average Zacks Rank (265 out of 265) would place in the bottom 1%.

The Zacks Sector Rank assigns a rating to each of the 16 Sectors based on their average Zacks Rank.

A sector with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The sector with the best average Zacks Rank would be considered the top sector (1 out of 16), which would place it in the top 1% of Zacks Ranked Sectors. The sector with the worst average Zacks Rank (16 out of 16) would place in the bottom 1%.

The Style Scores are a complementary set of indicators to use alongside the Zacks Rank. It allows the user to better focus on the stocks that are the best fit for his or her personal trading style.

The scores are based on the trading styles of Value, Growth, and Momentum. There's also a VGM Score ('V' for Value, 'G' for Growth and 'M' for Momentum), which combines the weighted average of the individual style scores into one score.

Value ScoreA

Growth ScoreA

Momentum ScoreA

VGM ScoreA

Within each Score, stocks are graded into five groups: A, B, C, D and F. As you might remember from your school days, an A, is better than a B; a B is better than a C; a C is better than a D; and a D is better than an F.

As an investor, you want to buy stocks with the highest probability of success. That means you want to buy stocks with a Zacks Rank #1 or #2, Strong Buy or Buy, which also has a Score of an A or a B in your personal trading style.

Zacks Earnings ESP (Expected Surprise Prediction) looks to find companies that have recently seen positive earnings estimate revision activity. The idea is that more recent information is, generally speaking, more accurate and can be a better predictor of the future, which can give investors an advantage in earnings season.

The technique has proven to be very useful for finding positive surprises. In fact, when combining a Zacks Rank #3 or better and a positive Earnings ESP, stocks produced a positive surprise 70% of the time, while they also saw 28.3% annual returns on average, according to our 10 year backtest.

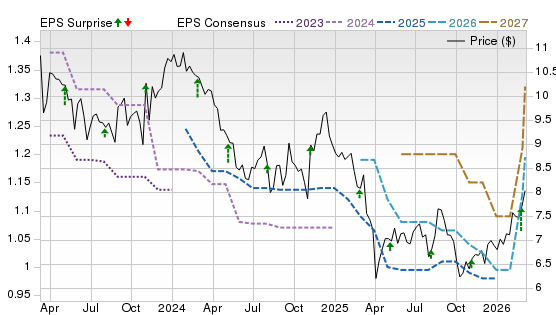

Air France-KLM is a European network carrier with a $3.05 billion market cap, operating Air France, KLM and Transavia alongside a maintenance arm. In 2025, the group grew revenue to €33 billion and delivered an operating result of €2 billion, reflecting stronger premium demand and tighter cost control. That momentum, paired with a low-multiple valuation, is why the ADR can look “cheap” despite a choppy macro backdrop.

Potential Risks

Airlines are exposed to fuel, labor and airport-charge inflation, plus FX moves. Disruptions can be expensive: management flagged a roughly €90 million hit tied to Amsterdam de-icing, while geopolitics and airspace restrictions can pressure unit costs.

Forecast

A Zacks Rank #1, A for Value and Growth and B for Momentum, indicate improving expectations. The chart shows 2026–2027 EPS consensus stair-stepping higher after mostly positive surprises, suggesting room for further upward revisions if demand and reliability hold.

This is our short term rating system that serves as a timeliness indicator for stocks over the next 1 to 3 months. How good is it? See rankings and related performance below.

The Zacks Industry Rank assigns a rating to each of the 265 X (Expanded) Industries based on their average Zacks Rank.

An industry with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The industry with the best average Zacks Rank would be considered the top industry (1 out of 265), which would place it in the top 1% of Zacks Ranked Industries. The industry with the worst average Zacks Rank (265 out of 265) would place in the bottom 1%.

The Zacks Sector Rank assigns a rating to each of the 16 Sectors based on their average Zacks Rank.

A sector with a larger percentage of Zacks Rank #1's and #2's will have a better average Zacks Rank than one with a larger percentage of Zacks Rank #4's and #5's.

The sector with the best average Zacks Rank would be considered the top sector (1 out of 16), which would place it in the top 1% of Zacks Ranked Sectors. The sector with the worst average Zacks Rank (16 out of 16) would place in the bottom 1%.

The Style Scores are a complementary set of indicators to use alongside the Zacks Rank. It allows the user to better focus on the stocks that are the best fit for his or her personal trading style.

The scores are based on the trading styles of Value, Growth, and Momentum. There's also a VGM Score ('V' for Value, 'G' for Growth and 'M' for Momentum), which combines the weighted average of the individual style scores into one score.

Value ScoreA

Growth ScoreA

Momentum ScoreA

VGM ScoreA

Within each Score, stocks are graded into five groups: A, B, C, D and F. As you might remember from your school days, an A, is better than a B; a B is better than a C; a C is better than a D; and a D is better than an F.

As an investor, you want to buy stocks with the highest probability of success. That means you want to buy stocks with a Zacks Rank #1 or #2, Strong Buy or Buy, which also has a Score of an A or a B in your personal trading style.

Zacks Earnings ESP (Expected Surprise Prediction) looks to find companies that have recently seen positive earnings estimate revision activity. The idea is that more recent information is, generally speaking, more accurate and can be a better predictor of the future, which can give investors an advantage in earnings season.

The technique has proven to be very useful for finding positive surprises. In fact, when combining a Zacks Rank #3 or better and a positive Earnings ESP, stocks produced a positive surprise 70% of the time, while they also saw 28.3% annual returns on average, according to our 10 year backtest.

Alto Ingredients is a small-cap producer of specialty alcohols, renewable fuels and essential ingredients with a $355.8 million market cap. In Q4 2025, management highlighted strong execution and a milestone in its strategic realignment, which is important because a richer mix of specialty alcohols can reduce sensitivity to fuel margins over time. Rising renewable fuel exports will be a major positive.

Potential Risks

Results still hinge on corn, energy and ethanol pricing, plant reliability and logistics. Changes in biofuel policy, weak gasoline demand, or a squeeze in co-products can put pressure on cash flow.

Forecast

A Zacks Rank #1 indicates that estimates are trending higher. A Value Score of C is less forceful, but Growth and Momentum Scores of A point to improving fundamentals and trend. The chart shows consensus turning up into 2026–2027 after a recent beat, a backdrop that can fuel more revisions.

The Zacks Rank is a proprietary stock-rating model that uses trends in earnings estimate revisions and earnings-per-share (EPS) surprises to classify stocks into five groups: #1 (Strong Buy), #2 (Buy), #3 (Hold), #4 (Sell) and #5 (Strong Sell). The Zacks Rank is calculated through four primary factors related to earnings estimates: analysts' consensus on earnings estimate revisions, the magnitude of revision change, the upside potential and estimate surprise (or the degree in which earnings per share deviated from the previous quarter).

Zacks builds the data from 3,000 analysts at over 150 different brokerage firms. The average yearly gain for Zacks Rank #1 (Strong Buy) stocks is +23.62% per year from January, 1988, through June 2, 2025.

Selections for Best Cheap Stocks Under $10 are based on the current top ranking stocks based on Zacks Indicator Score, Style Scores and fundamentals. For this list, only companies that have average daily trading volumes of 100,000 shares or more were considered, as well as companies from the top 50% of all industries. All information is current as of market open, March 11, 2026.

General Questions About Cheap Stocks

What are the Benefits of Buying Cheap Stocks?

Cheap stocks can make investing more accessible, especially for investors who don’t want to commit large sums to a single position. Because these stocks trade at lower prices, investors can spread their capital across multiple companies, sectors, or strategies, helping improve diversification.

In addition, many stocks fall below $10 not because the underlying business is broken, but because of temporary challenges such as economic slowdowns, industry cycles, earnings volatility, or broader market sell-offs. When conditions improve, these stocks may rebound sharply, offering attractive upside potential. Cheap stocks can also provide exposure to undervalued or overlooked sectors that are out of favor but poised for recovery.

The primary risk with cheap stocks is that their low price may reflect genuine business problems rather than temporary setbacks. These companies often experience higher volatility, meaning prices can swing sharply in either direction. Many also have weaker balance sheets, higher debt loads, or limited cash reserves, making them more vulnerable during economic downturns.

Additionally, cheap stocks may face challenges raising capital, maintaining profitability, or competing with larger rivals. Without careful analysis, investors risk buying into so-called “value traps” — stocks that appear inexpensive but continue to decline because fundamentals fail to improve.

Can Cheap Stocks Actually Make Money?

Yes, cheap stocks can generate meaningful returns when purchased at the right time and for the right reasons. Numerous well-known companies have traded below $10 during periods of market stress, corporate restructuring, or industry downturns before eventually recovering.

That said, success is far from guaranteed. Cheap stocks tend to require patience, a willingness to tolerate volatility, and a focus on long-term business trends rather than short-term price movements.

Are Cheap Stocks a Good Investment for Beginners?

Cheap stocks can be suitable for beginners if approached cautiously. Their lower price points allow new investors to learn portfolio management, diversification, and risk control without committing excessive capital.

However, beginners should avoid concentrating too much money in a single cheap stock or chasing speculative names purely because they look inexpensive. Focusing on established companies, clear business models, and basic fundamentals can help reduce risk while building investing experience.

What is the Difference Between Cheap Stocks and Penny Stocks?

Cheap stocks generally trade under $10 but are listed on major exchanges like the NYSE or Nasdaq and are required to meet stricter regulatory and reporting standards. Penny stocks, by contrast, often trade under $5 — and frequently under $1 — and are commonly found on over-the-counter (OTC) markets.

Penny stocks typically carry far higher risk due to low liquidity, limited transparency, and greater susceptibility to manipulation. While some cheap stocks are speculative, they usually offer better disclosure and stability than penny stocks.

How to Select Fundamentally Strong Cheap Stocks

How can I Analyze a Cheap Stock's Potential?

Analyzing a cheap stock starts with examining its financial health and business model. Key areas to review include revenue growth trends, profitability or progress toward profitability, debt levels, and cash flow generation. Investors should also evaluate the company’s competitive position within its industry, the durability of its products or services, and management’s long-term strategy.

Beyond the numbers, it’s important to consider industry tailwinds, upcoming catalysts such as new products or restructuring efforts, and whether the company has a credible path to improving performance.

How do I Know if a Stock is Cheap or Just Bad?

A truly cheap stock trades at a low valuation relative to its future earnings potential, assets, or cash flow, often due to temporary challenges. These companies usually have a realistic plan for recovery, cost control, or growth.

A bad stock, on the other hand, lacks earnings visibility, suffers from persistent losses, carries excessive debt, or operates in a declining or obsolete industry. If management cannot articulate a clear strategy for improvement, or if fundamentals continue to deteriorate, the stock may remain cheap for the wrong reasons.

Strategy and Portfolio Building with Cheap Stocks

Is it Better to Buy 100 Shares of a Cheap Stock, or 1 Share of an Expensive Stock?

The number of shares owned is largely irrelevant. What matters is the percentage return on investment and the level of risk taken. A single share of a high-quality company can outperform hundreds of shares of a struggling business. Investors should focus on expected returns, downside risk, and how each position fits within the broader portfolio.

How do I Build a Diversified Portfolio Using Cheap Stocks?

Diversification with cheap stocks involves spreading investments across multiple sectors, industries, and business models. Combining growth-oriented names with income or value stocks can help balance risk and reward. Limiting position sizes — especially for more speculative companies — helps prevent any single stock from dominating portfolio performance.

How can I Screen for Cheap Stocks with Growth Potential?

Investors can use stock screeners to identify candidates by filtering for price, market capitalization, revenue growth, manageable debt levels, and improving margins. Additional filters such as analyst earnings revisions, insider buying, or strong free cash flow can further refine results. Screening helps narrow the field, but deeper research is still essential before investing.

Cheap Stock Investing Through ETFs

What are Some Good ETFs that Hold Cheap or Value Stocks?

Investors who prefer diversification over picking individual stocks may consider value-focused ETFs. Examples include:

Vanguard Value ETF (VTV).

iShares Russell 2000 Value ETF (IWN).

SPDR Portfolio S&P 600 Small Cap Value ETF (SLYV).

These funds hold baskets of undervalued stocks across multiple sectors and market capitalizations. ETFs can reduce single-stock risk while still providing exposure to companies trading at attractive valuations.

Strong Buy

Strong Buy

Hold

Hold